Weekly Macro Focus - CW 21

Debt Gravity – Refinancing Pressure and America's Fiscal Drift

While China-based trade deals push equities toward all-time highs again, America’s fiscal foundation is quietly eroding beneath the surface. Record refinancing needs, surging interest costs, and a lack of political will for structural reform are creating a new pressure regime in the bond market. Add to that a fresh downgrade by Moody’s—and a costly fiscal proposal dubbed “The Big Beautiful Bill”—and the risks to U.S. creditworthiness are accelerating fast.

❗ $9.2 Trillion to Refinance in 2025

The U.S. government faces a sharp test this year: over $9.2 trillion in Treasury debt is maturing, more than one-third of all marketable debt. This needs to be rolled over in a far higher rate environment than when it was first issued.

The average interest rate on federal debt has risen from 1.4% (2021) to over 3.2% (2025). As more low-rate debt is replaced with high-cost refinancing, annual interest expenses are projected to exceed $1 trillion by 2026—greater than the entire U.S. defense budget.

The core problem: America borrows more to pay for past borrowing, and that borrowing is getting increasingly expensive.

🏛️ Trump’s Fiscal Agenda: The Big Beautiful Bill

Donald Trump’s “Big Beautiful Bill,” gaining traction in the House, proposes:

Making the 2017 tax cuts permanent

Imposing a 10% universal tariff on all imports

Providing tax breaks for capital-intensive firms—especially those in real estate, construction, and machinery-heavy industries

These policies may support short-term domestic production, but they risk expanding the primary deficit, especially when paired with higher import costs and slower global trade.

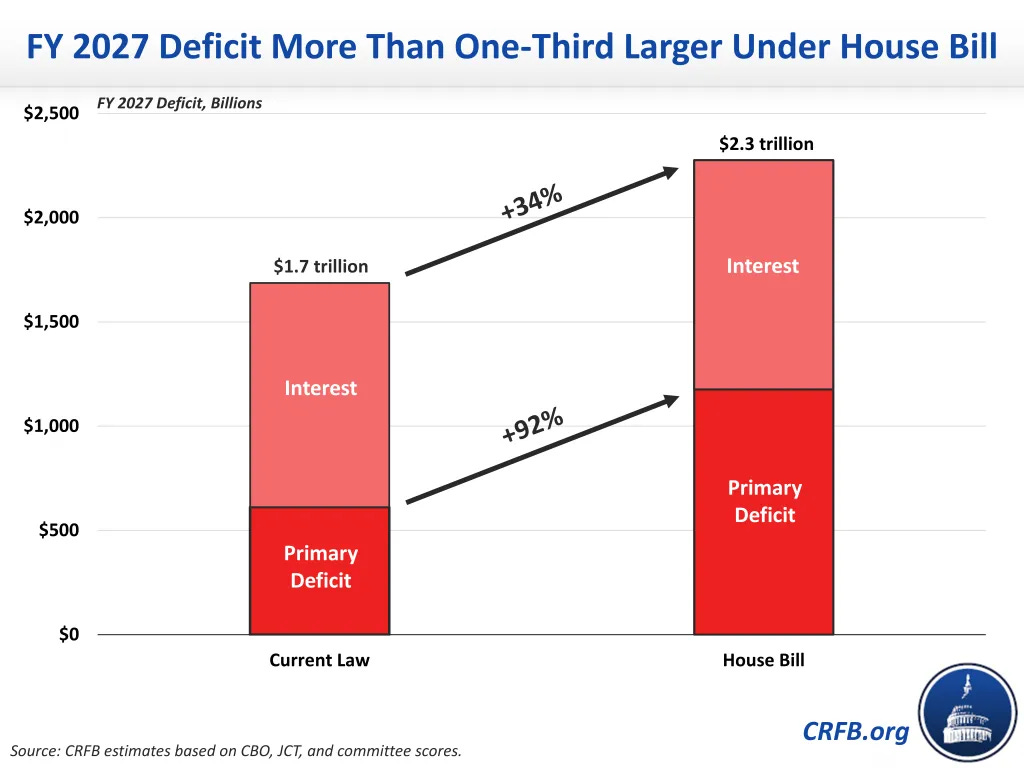

📉 Deficits in Focus – And Visualized

According to the Committee for a Responsible Federal Budget (CRFB), if Trump-aligned policies pass:

The FY 2027 deficit would rise to $2.3 trillion, up from $1.7 trillion under current law

The primary deficit (excluding interest) would nearly double—growing +92%

In short: the U.S. deficit picture could deteriorate even faster than expected, with debt service compounding the pressure.

📊 Market Response: Yields Rise, Dollar Slips

The Treasury market has begun to react:

10-year yields are pushing toward 5%

The U.S. dollar has weakened, despite elevated interest rates

This is an unusual signal: yields typically rise on economic strength. But in this case, they’re rising on fiscal risk concerns—suggesting investors are demanding more compensation for holding U.S. debt.

⚠️ Why Moody’s Downgrade Didn’t Shock Markets – But Still Matters

Last Friday, Moody’s downgraded the U.S. credit rating—joining S&P (2011) and Fitch (2023), who had already taken this step years earlier.

So why didn’t markets react more forcefully?

Because two of the three major agencies had already downgraded the U.S.. Moody’s move simply aligned with what markets had long priced in.

However, the timing of the downgrade was symbolic. Moody’s explicitly cited the growing fiscal imbalance—and many analysts view it as a direct critique of the widening deficit projections under Trump’s “Big Beautiful Bill.”

In essence, while the downgrade wasn’t a market shock, it added official weight to growing concerns about America’s fiscal trajectory.

🔧 Can This Be Fixed?

Raising the debt ceiling is not a solution—it merely postpones confrontation with the underlying issue: structural deficits in a high-rate world.

What would a solution look like?

Extending debt maturities to reduce near-term refinancing exposure (currently difficult due to high yields)

Modernizing the tax code by closing loopholes, not just cutting rates

Restructuring entitlements gradually to control long-term costs

Boosting real productivity growth through infrastructure, innovation, and education

Implementing automatic stabilizers (spending or tax rules tied to the business cycle)

But all of these require political consensus—something in short supply.

🧩 Conclusion: A System Under Strain

America isn’t out of funding options, but it is running out of fiscal slack. The refinancing wave, rising rates, deficit expansion, and shifting credit ratings are converging. Markets are watching—and responding.

The coming months will test whether the U.S. is still seen as the ultimate safe haven, or whether that narrative begins to quietly shift.

Stay informed and unlock alpha with Gauch-Research. 🚀