SVC-Update

Weekly Recap & Outlook

No financial advice.

Markets past week have once again been driven almost entirely by headlines, shifting rapidly from optimism to reality and back again. In such an environment, maintaining a clear and structured view becomes increasingly difficult. The goal of this update is therefore to cut through the noise and refocus on what actually matters.

The conflict continues to escalate, and according to recent statements, no meaningful de-escalation is expected over the next 2 to 3 weeks. If anything, the risk leans toward further escalation.

From a market perspective, the key issue remains the disruption of critical trade routes. The Strait of Hormuz continues to see severely restricted traffic, effectively removing a major artery of global energy supply from the market.

As highlighted in previous updates, even in the case of a ceasefire or negotiated resolution, the structural damage has already been done. Energy infrastructure destruction and ongoing supply chain disruptions will continue to have lasting effects.

Another critical risk lies in the Bab el-Mandeb strait. A potential blockade by the Houthis could have significant consequences. Oil prices could increase by an additional 20 dollars per barrel. Around 12 percent of global trade would be affected. Delivery times for goods could extend by 10 to 14 days. This would further intensify existing supply chain stress and amplify inflationary pressures globally.

With headlines remaining unreliable, the following dates are far more relevant in determining the direction of the coming months:

April 10 marks the expiry of the US exemption for purchasing Russian crude oil. If this is not extended, additional supply will be removed from an already constrained market.

April 15 is the estimated depletion point of around 400 million barrels of strategic reserves. This would mark the largest SPR drawdown in IEA history and leave no meaningful emergency buffer.

April 30 represents the expiration of all emergency measures.

Once these deadlines pass, the market effectively approaches a cliff scenario without a safety net. Even a late resolution would likely come too late to prevent structural imbalances. In such a case, the current disconnect between futures, which are trading at a discount, and spot prices in the oil market is unlikely to persist. A repricing higher in futures would invalidate the current hope driven positioning.

Given the current uncertainty, risk management remains critical. The base case remains skewed toward further escalation. However, the outlook would need to be reassessed in case of a confirmed ceasefire or a clear end of the conflict, as well as a reopening of the Strait of Hormuz.

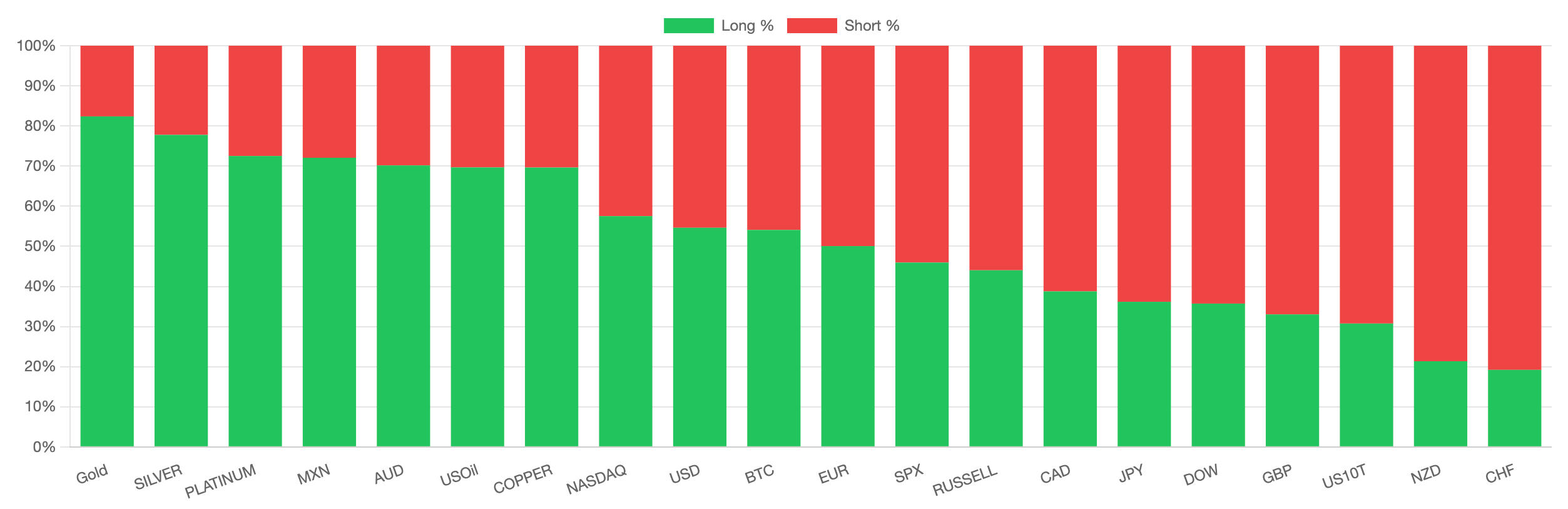

Institutional Positioning

Below is a snapshot of current large speculator positioning, based on proprietary tools designed to visualize flows in a simplified and structured way.

Overall Positioning

Summary Update April 3

Beyond geopolitics, recent macro data added another layer of complexity.

News Recap

Non-Farm Employment Change (Previous: -133K, Forecast: 65K, Actual: 178K):

The US economy added 178K jobs in March 2026, marking the strongest increase since December 2024. This follows a revised decline of 133K in February, which was largely impacted by a strike in the healthcare sector. The latest figure came in well above market expectations of 65K. Job growth was heavily concentrated in healthcare, which added 76K jobs. Within that, ambulatory health care services accounted for 54K, including a 35K increase in offices of physicians as workers returned from strike-related disruptions. Construction added 26K jobs following weather-related declines during the winter months. Transportation and warehousing contributed 21K jobs, manufacturing added 15K, and social assistance continued its upward trend with an increase of 14K.On the downside, federal government employment declined by 18K, while financial activities saw a decrease of 15K. Revisions to prior data show that January payrolls were adjusted higher by 34K to 160K, while February was revised lower by 41K to -133K. Combined, employment for the two months is now 7K lower than previously reported.

The unemployment rate declined to 4.3 percent in March from 4.4 percent in February, coming in below expectations of 4.4 percent. The number of unemployed individuals decreased by 332,000 to 7.239 million. However, total employment fell by 64,000 to 162.85 million, while the labor force declined by 396,000 to 170.09 million. This pushed the participation rate down by 0.1 percentage point to 61.9 percent. At the same time, the broader U-6 unemployment rate, which includes discouraged and underemployed workers, increased to 8 percent from 7.9 percent.

The key takeaway is that this was a misleadingly strong print. The labor market is showing further signs of softening.

US Final Services PMI (Previous: 51.1, Forecast: 51.5, Actual: 49.8):

The S&P Global US Services PMI fell to 49.8 in March 2026 from 51.7 in the previous month and was revised down from the preliminary estimate of 51.1. This marks the first contraction in the services sector in over three years. The decline was driven by the weakest growth in new business since April 2024, as firms reported reduced client confidence and softer demand. This was partly linked to the impact of the Middle East conflict. Export activity deteriorated further, with tariffs and geopolitical tensions continuing to weigh on trade. Business sentiment weakened to a five-month low, as rising energy costs increased concerns around inflation and consumer spending. Employment edged lower for the first time since December, reflecting growing caution among firms. At the same time, input cost inflation accelerated to its highest level this year, largely driven by higher energy prices. Companies continued to pass these rising costs on to clients, pushing selling price inflation to an eight-month high.

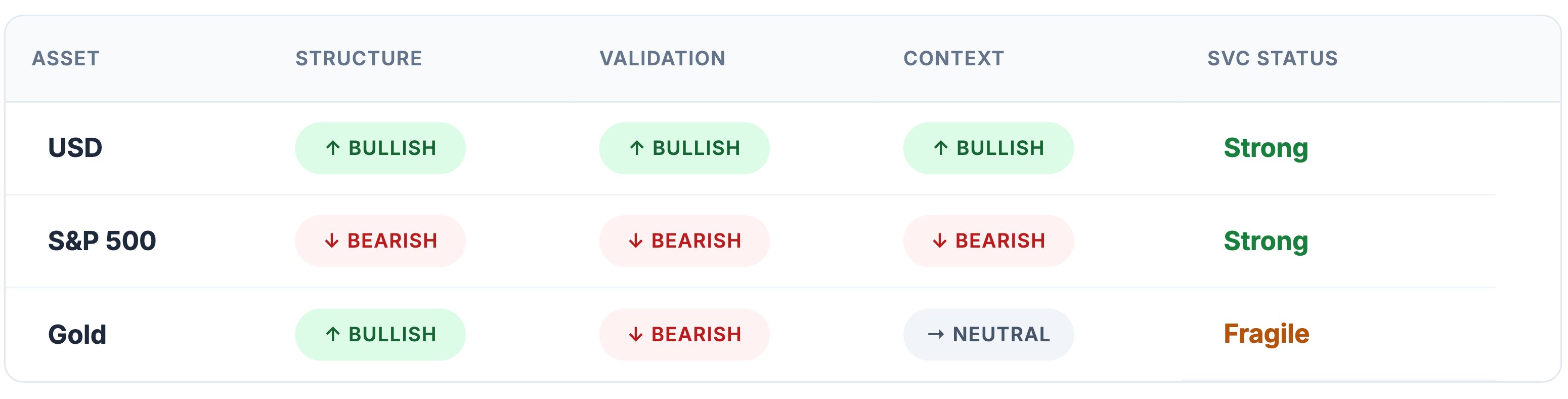

SVC Breakdown

USD

The dollar remains the most dominant in the current environment, supported by global demand and safe haven flows.

Gold

Gold has stabilized following the recent selloff. A further corrective move toward the 4900 region remains a realistic scenario.

S&P 500

Equities have shown notable resilience so far, largely driven by intermittent optimism. However, the combination of escalating geopolitical risks, tightening supply conditions and upcoming macro deadlines creates a fragile setup. A continuation of escalation, especially in combination with the outlined deadlines, could act as a catalyst for further downside in equities.

Upcoming News

ISM Services PMI

Core PCE Price Index

Final GDP

CPI

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research