SVC-Update

Weekly Recap & Outlook

Overview

No financial advice.

On Tuesday (Monday was a US holiday), the S&P 500 suffered its first drop of slightly more than -2% in quite some time, only to recover almost the entire move over the following days. The trigger for this short-lived equity rollercoaster was, unsurprisingly, new tariff threats from the US administration against several European countries, linked to the ongoing Greenland discussion. From a market perspective, however, the episode was resolved fairly quickly after President Trump and NATO Secretary General Mark Rutte reached a basic understanding on the Greenland issue.

While no concrete details were officially disclosed, reports from the New York Times suggest that the US could receive territorial rights in Greenland for the construction of military bases and broader military infrastructure. Mining rights are also said to be part of the discussions. It is worth noting that the existing agreement with Denmark and Greenland already allowed the US to establish military bases. What would be new, however, is the potential transfer of actual territory to the United States. Interestingly, this appears to be primarily a deal between Trump and Rutte/NATO, with Greenland’s local population reportedly not being consulted. From a market standpoint, though, the issue seems to be priced as “done for now,” as reflected by the swift recovery in equities.

While bond yields barely reacted to these developments, the US dollar weakened noticeably against the euro on a weekly basis. This move is likely driven by rumors that the US could support Japan in strengthening the yen, as well as speculation that BlackRock CIO Rick Rieder has emerged as a frontrunner for the eventual succession of Jerome Powell at the Fed.

In addition, we received several data releases this week, which I will break down below:

Final GDP q/q (Previous: 4.3%, Forecast: 4.3%, Actual: 4.4%):

The economy grew at an annualized 4.4%, above the initial 4.3% estimate and the fastest pace since Q3 2023. Growth was driven by solid consumer spending (+3.5%), a sharp export rebound (+9.6%), higher government spending, and a much smaller drag from inventories. The main soft spot was fixed investment, which rose just 0.8%, down from 4.4% in Q2, suggesting that business investment remains sluggish despite strong headline growth.

Core PCE Price Index m/m (Previous: 0.2%, Forecast: 0.2%, Actual: 0.2%):

US core PCE inflation rose unchanged from October and in line with expectations. On a year-over-year basis, core inflation edged up slightly to 2.8% from 2.7%, also exactly as forecast, offering little new information for the near-term Fed outlook.

Flash Manufacturing PMI m/m (Previous: 51.8, Forecast: 51.9, Actual: 51.9):

The S&P Global Manufacturing PMI edged up to 51.9 from 51.8, broadly in line with expectations. While output growth accelerated to its strongest pace since August and new orders rebounded, overall momentum remained weak, with employment growth slowing to a six-month low, pointing to a still fragile recovery in factory activity.

Flash Services PMI m/m (Previous: 52.5, Forecast: 52.9, Actual: 52.5):

The S&P Global Services PMI held at 52.5, below expectations, marking nearly three years of uninterrupted expansion. However, new business growth slowed, exports fell at the fastest pace since 2022, and employment growth eased, reflecting softer demand. While input cost inflation moderated and price pressures cooled slightly, business confidence declined to a three-month low, suggesting the services sector is still expanding, but with fading tailwinds.

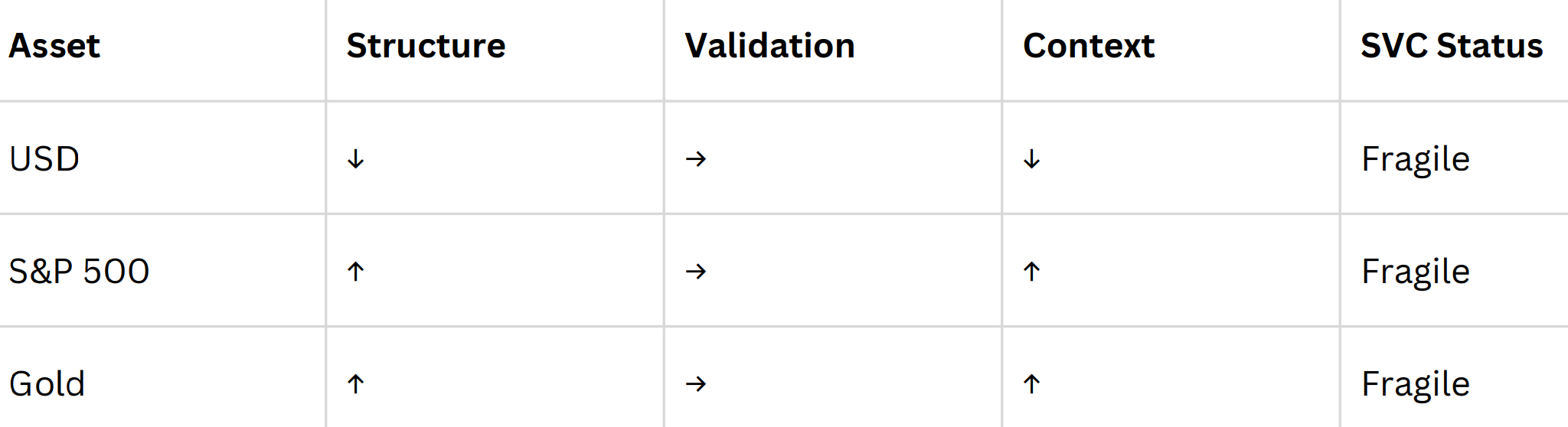

SVC Breakdown

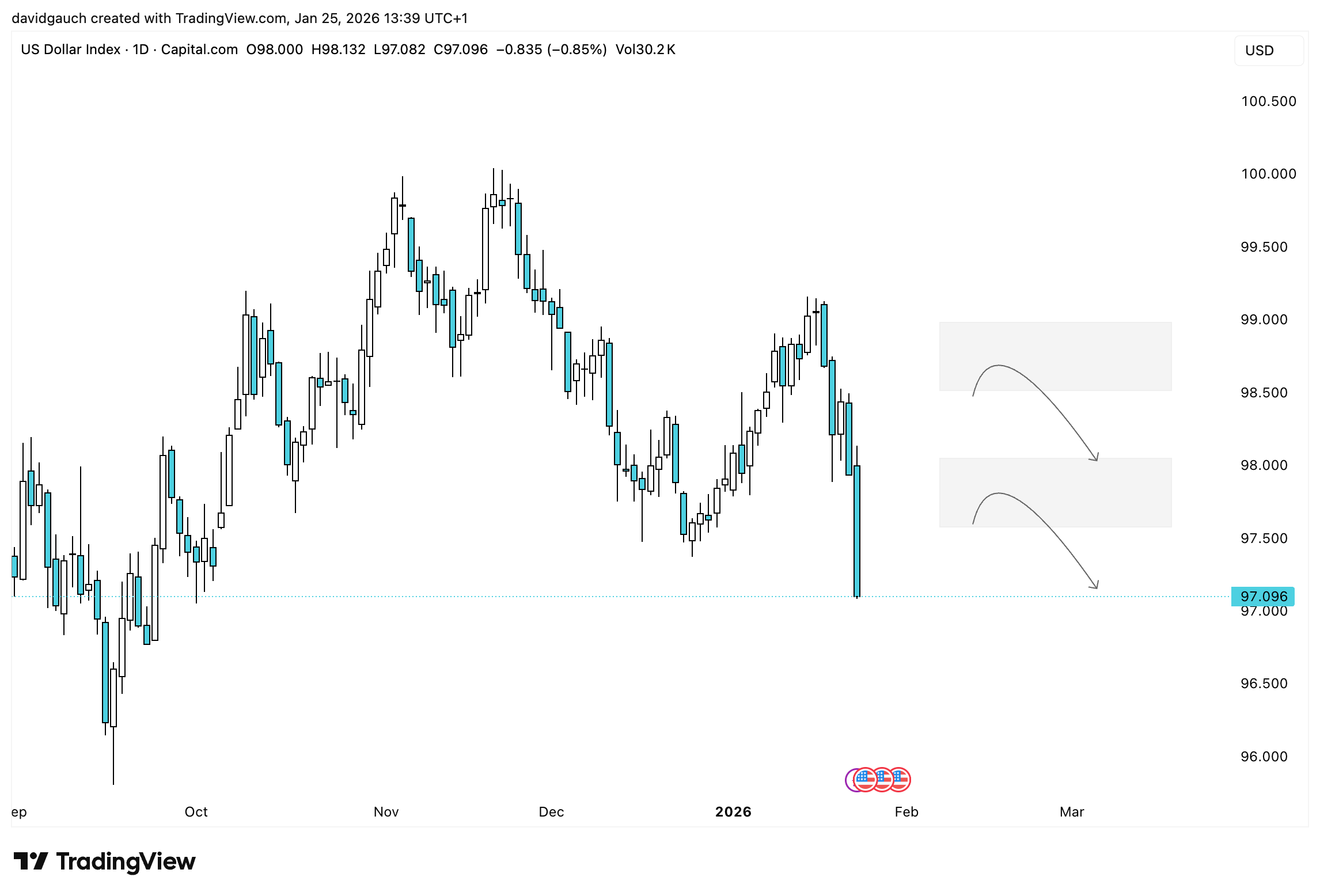

USD

Despite relatively stable data this week, the prior market structure could not be maintained. This raises the risk that the longer-term bearish structure is resuming. As our SVC framework does not yet provide a strong read, positioning should be limited to reduced-risk setups only.

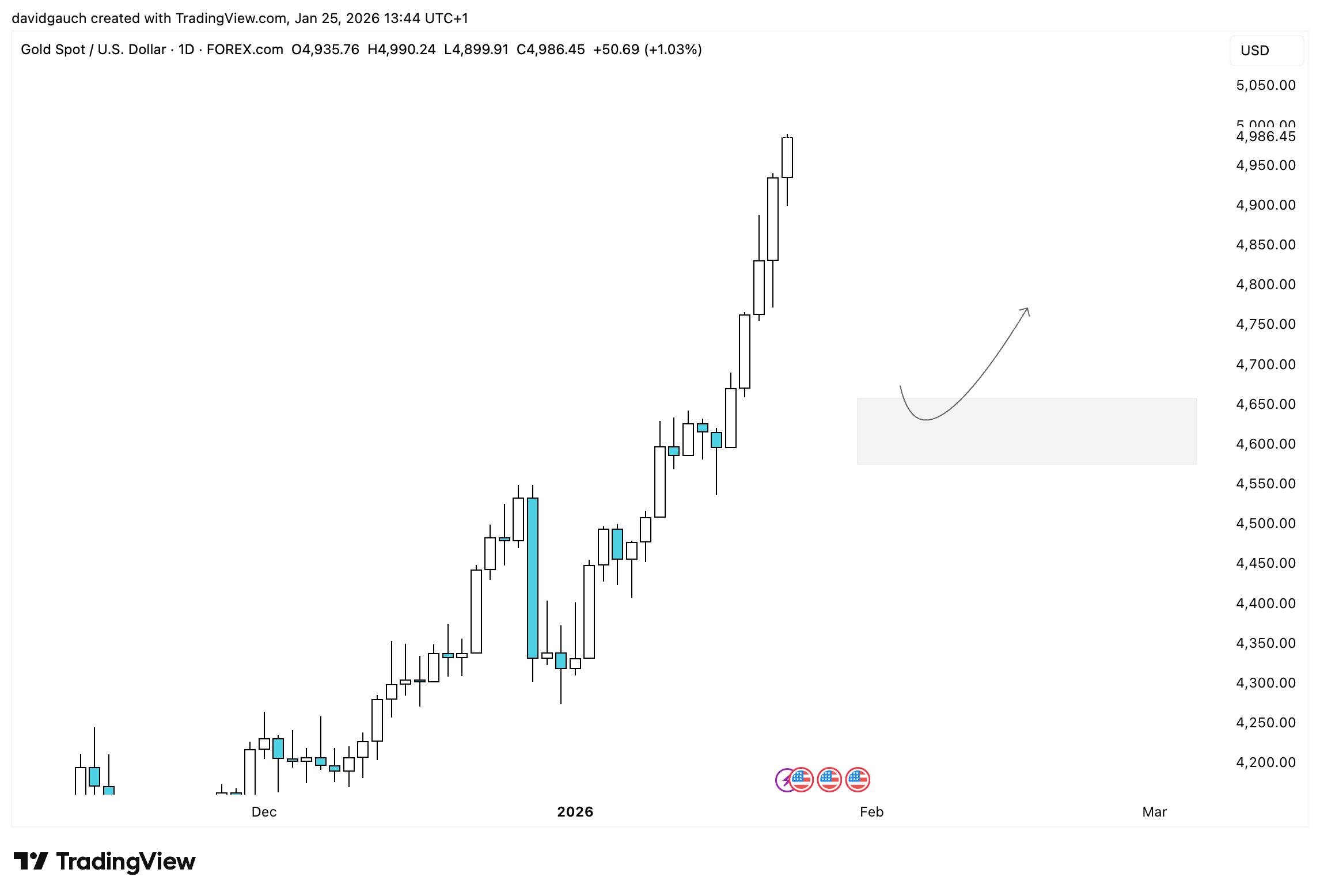

Gold

Gold and silver closed the week with an impressive rally, supported by a weaker US dollar. Silver pushed above the 100 level, while gold advanced to just shy of 5,000. Members of our premium chat were able to benefit from additional long setups in gold during the move. With no attractive entry opportunities available at the moment, it makes sense to wait for the next retracement before considering new positions.

US500

The recent “TACO trades” have once again provided attractive entry opportunities in the S&P, as demonstrated well this week. Partially supported by our SVC-Framework, the S&P remains a bullish signal. That said, upcoming earnings releases this week are an important risk factor and could reintroduce short-term volatility into the market.

Upcoming News

Federal Funds Rate / FOMC Press Conference

Earnings: ASML, MSFT, META, TSLA, MC, VISA

PPI

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research