SVC-Update

Weekly Recap & Outlook

Before we begin, I would like to share my free Telegram channel, where I post daily market insights, news updates, and my personal trading ideas. If you’re interested, you can join using the link below:

No financial advice.

Hi everyone and welcome back to this week’s SVC-Update after what felt like a rather chaotic week in terms of market dynamics.

While intraday and daily price action picked up noticeably compared to the past few months, many major indices actually held up surprisingly well when viewed on a weekly basis.

US and Chinese large caps remained relatively stable overall. At the same time, one rule that has often held true in recent years proved itself once again: whenever global uncertainty rises, European equity markets tend to feel the impact the most.

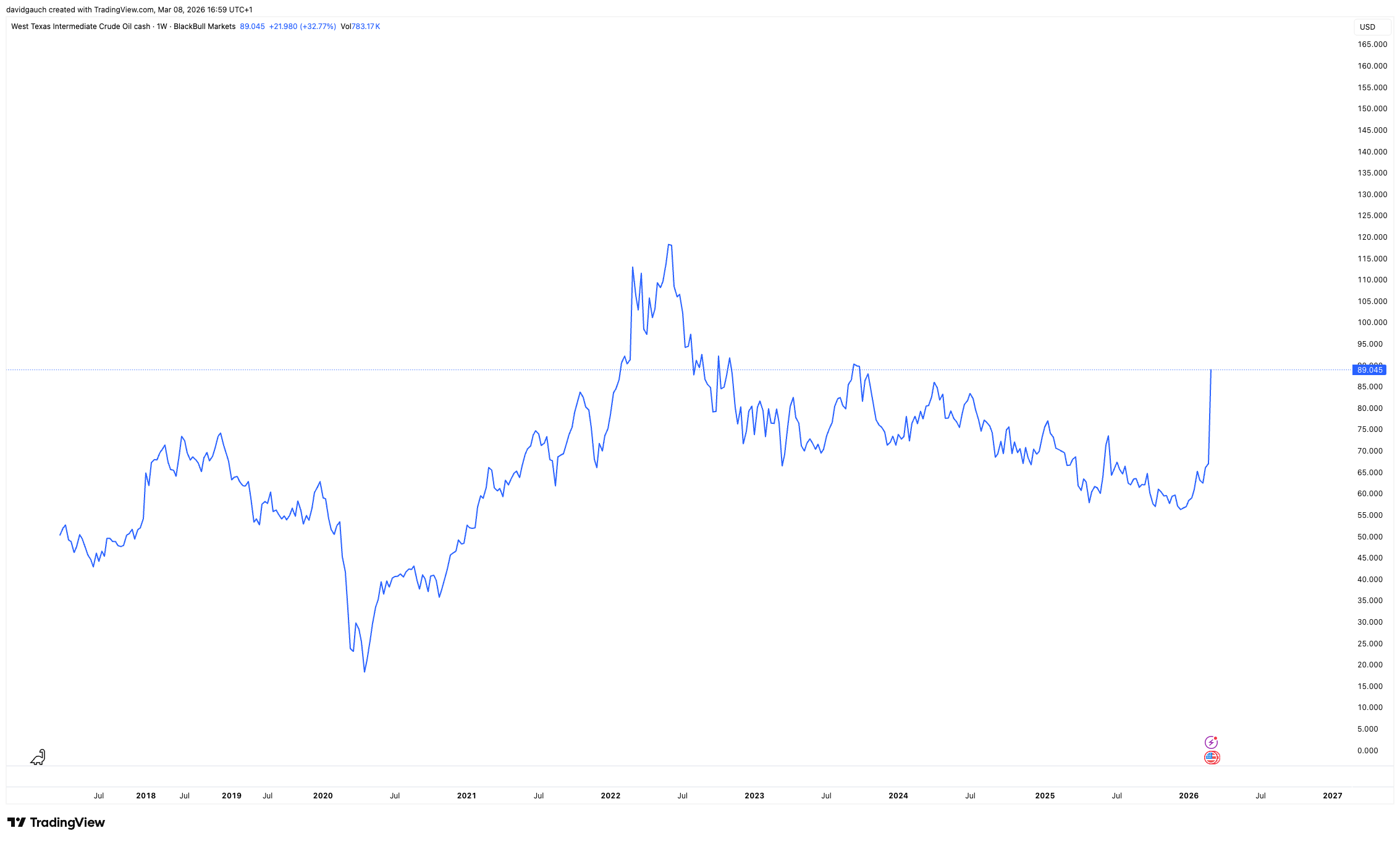

Oil moves back into focus

Outside of equities, oil clearly stood out this week. A +32% weekly move in WTI is certainly significant. That said, it is worth remembering that we have seen even more extreme levels during previous episodes in recent years.

For private consumers, however, the raw oil price itself is less relevant than what ultimately shows up at the gas station. And while we are indeed seeing a spike in US gasoline prices, they are still lagging behind the peaks observed in 2023 and 2024.

During earlier oil crises, crude oil accounted for roughly one quarter of global electricity production. Today that share has fallen to low single digits. As a result, spikes in oil prices no longer automatically translate into sharp spikes in electricity prices.

This becomes quite visible when looking at current German electricity prices, which have remained relatively contained despite the recent oil move.

Taken together, it suggests that, despite some alarming headlines, we are still far away from a genuine energy crisis.

Rising yields and central bank concerns

Another development many market participants likely noticed is the sharp move higher in global bond yields.

The underlying concern in the market is that higher energy prices could force central banks to move more slowly when it comes to rate cuts. In the case of the Federal Reserve, this could mean delaying easing cycles, while in the Eurozone some investors even speculate about the possibility that the ECB might have to reconsider tightening again. However, I would be cautious with that interpretation.

First, it is far from guaranteed that an oil price spike necessarily translates into a meaningful rise in core inflation. And second, the duration of the current geopolitical conflict remains highly uncertain, even though the current news flow suggests it could persist for longer.

Corporate fundamentals remain strong

If we momentarily put geopolitics aside, the picture at the corporate level actually continues to look very solid. The earnings season, which is now largely completed, once again came in well above expectations. On an index level, the S&P 500 recorded its sixth consecutive quarter of double-digit earnings growth, highlighting that corporate fundamentals remain robust.

There was, however, a small downside surprise at the end of the week: Friday’s US labor market data came in weaker than expected. That said, the 92k jobs lost can at least partly be attributed to one-off effects, which means the data point should be interpreted with some caution rather than as a clear signal of a broader deterioration in the labor market. More on that down below.

News Recap

US Non-Farm Employment Change (Previous: 126K, Forecast: 58K, Actual: -92K):

The US economy shed 92k jobs in February, marking the largest decline in roughly four months. This compares to a downwardly revised gain of 126k jobs in January and came in well below consensus expectations, which had anticipated an increase of around 59k jobs. At first glance, the headline number certainly looks concerning. However, the underlying details paint a somewhat more nuanced picture.

A significant portion of the decline was concentrated in health care employment, which fell by 28k jobs, largely reflecting strike activity during the month. Within the sector, physicians’ offices lost 37k jobs, while hospital employment actually increased by 12k, highlighting the temporary nature of part of the weakness.

Elsewhere, several sectors continued to show softer momentum. Employment declined in information (-11k) and federal government (-10k), while additional losses were recorded in transportation and warehousing (-11k) as well as manufacturing (-12k).

At the same time, not all areas of the labor market weakened. Social assistance employment continued its steady upward trend, adding 9k jobs, driven primarily by individual and family services, which expanded by 12k positions.

In addition to the February figures, the report also included downward revisions to previous months. The December reading was revised from +48k to -17k, while January was adjusted slightly lower from +130k to +126k. Combined, these revisions reduce previously reported employment gains by 69k jobs.

Taken together, the latest data reinforces the picture that US payroll growth has been broadly flat throughout 2025, suggesting a labor market that is no longer accelerating but also not collapsing.

For policymakers and markets alike, the key question going forward will be whether this report marks the beginning of a more sustained slowdown — or merely reflects temporary distortions and sector-specific factors.

US ISM Services PMI (Previous: 53.8, Forecast: 53.5, Actual: 56.1):

The ISM Services PMI in the US rose to 56.1 in February 2026, up from 53.8 in January, exceeding market expectations of 53.5 and marking the strongest expansion in the sector since August 2022. The increase was mainly driven by stronger business activity, with the subindex climbing to 59.9 from 57.4, its highest level since September 2024.

New orders also showed solid momentum, rising to 58.6 from 53.1, representing the largest increase in 17 months. Meanwhile, the employment component improved to 51.8 from 50.3, indicating the fastest pace of job growth in the sector in about a year.

The Supplier Deliveries Index eased slightly to 53.9 from 54.2, but remained above 50 for the 15th consecutive month, signaling continued strong demand and slower delivery times.

At the same time, the Prices Index declined to 63, its lowest level since March 2025. While this suggests some easing in cost pressures, the reading remains well above 60, pointing to ongoing inflationary pressure in the services sector.

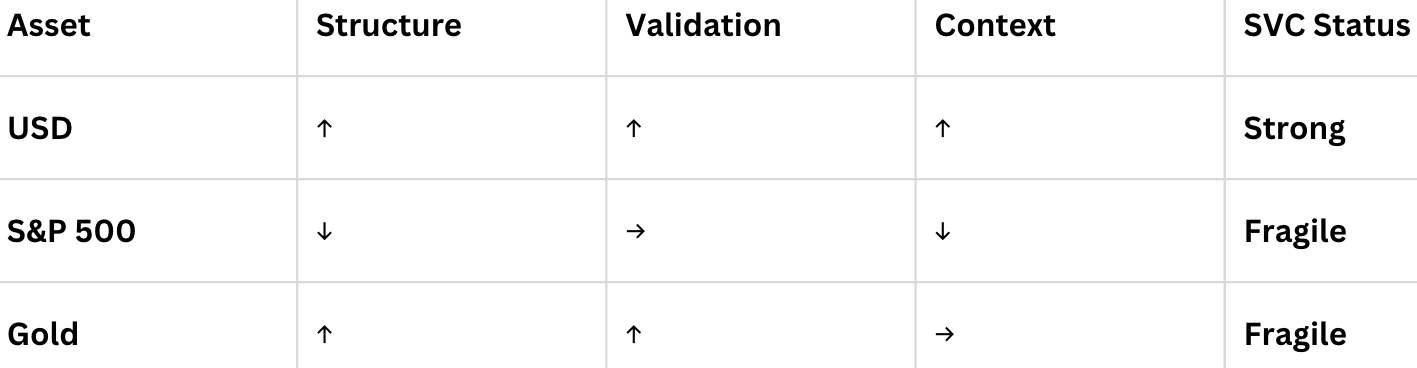

SVC Breakdown

USD

The last three SVC Updates each highlighted attractive long opportunities in the US Dollar, and the first upside target has now been reached. Amid ongoing geopolitical tensions and no visible signs of easing, the US Dollar continues to benefit from its role as a risk-off asset, particularly against more risk-sensitive currencies such as the EUR and NZD in this case.

Further Game Plan:

Gold

Gold traded more like a risk-off asset last week, experiencing several sharp sell-offs, which were likely also driven by the strength of the US Dollar. However, in an environment with a somewhat less volatile dollar, it could become attractive to position for potential long opportunities again.

S&P 500

As discussed in recent weeks, the key levels in the S&P 500 were well defined. We have now seen the first break below the gamma put support, meaning that market makers’ hedging positions were no longer able to support the market to the upside. In this environment, potential upside retracements could be used to establish short positions as a hedge within a long portfolio.

Upcoming News

Consumer Price Index

Core PCE Price Index m/m

Prelim GDP q/q

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research

It is refreshing to see macro analysis on substack. Keep up the great work!