SVC-Update

Weekly Recap & Outlook

Overview

No financial advice.

If you did not have the opportunity to follow markets last week, you can rest assured: you did not miss much at the headline level. The S&P 500 declined only 0.1% over the week, the VIX rose a moderate 1.8%, and 10-year yields moved roughly 4 basis points lower.

Beneath the surface, however, the situation was far more turbulent than the weekly performance might suggest. As Goldman Sachs recently described it, markets have been experiencing a form of “daily trench warfare.”

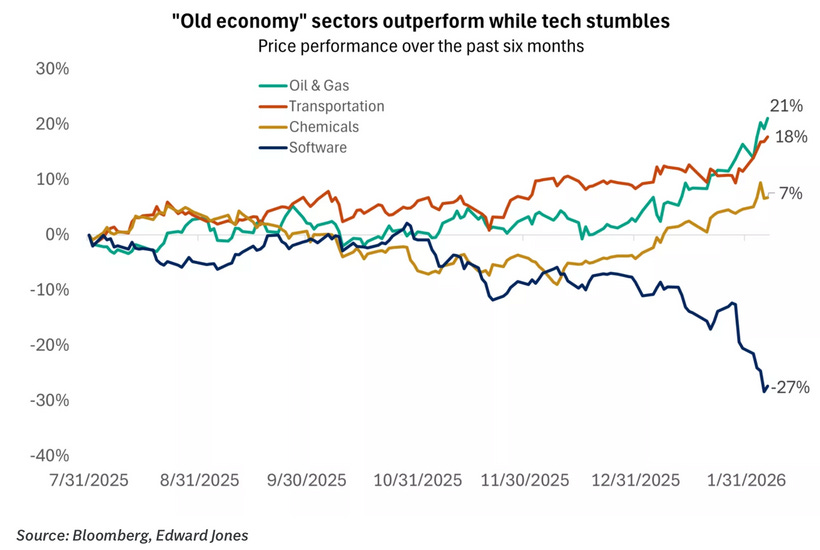

Without Friday’s sharp late-week rally in equities, the S&P 500 would have ended the week down more than 2.0%. At the same time, the sector rotation appears to be continuing, now reinforced by the narrative that advances in AI could ultimately render certain software business models obsolete, the so-called “SaaSpocalypse.” Edward Jones illustrates this dynamic effectively in the following chart:

Alongside this week’s volatility in equity markets and the delayed labour-market data, several additional economic releases were published, which are outlined below:

ISM Manufacturing PMI (Previous: 47.9, Forecast: 48.5, Actual: 52.6):

The US ISM Manufacturing PMI rose unexpectedly to 52.6 in January 2026, up from 47.9 in December and well above the consensus forecast of 48.5. The data indicate that manufacturing activity returned to expansion for the first time in twelve months, reaching its strongest level since 2022.

The improvement was broad-based, with notable gains in new orders (57.1 vs. 47.4), production (55.9 vs. 50.7), employment (48.1 vs. 44.8), supplier deliveries (54.4 vs. 50.8), and inventories (47.6 vs. 45.7). Despite the improvement, both the employment and inventory components remained in contraction territory. Price pressures were largely unchanged, with the prices index edging up slightly to 59 from 58.5.

According to Susan Spence, Chair of the ISM Manufacturing Business Survey Committee, the stronger headline reading should be interpreted with some caution. She noted that January is typically a restocking period following the holiday season, and some of the recent purchasing activity may reflect efforts to front-run anticipated price increases linked to ongoing tariff-related uncertainties.

ISM Services PMI (Previous: 54.4, Forecast: 53.5, Actual: 53.8):

The US ISM Services PMI held steady at 53.8 in January 2026, unchanged from the downwardly revised December reading and slightly above the consensus forecast of 53.5. The data point to continued solid expansion across the services sector.

Business activity strengthened notably, with the production index rising to 57.4 from 55.2. In contrast, momentum in other components moderated, as new orders eased to 53.1 from 56.5, employment edged down to 50.3 from 51.7, and supplier deliveries slowed to 54.2 from 51.8. Inventories (45.1 vs. 54.2) and the backlog of orders (44.0 vs. 42.6) remained in contraction territory, while price pressures increased, with the prices index climbing to 66.6 from 65.1.

According to Steve Miller, Chair of the ISM Services Business Survey Committee, respondent commentary in January increasingly focused on tariff-related impacts and broader uncertainty, likely reflecting annual contract renewals and geopolitical tensions. Energy products such as gasoline and diesel were still cited as declining in price. With the business activity and supplier deliveries indices reaching their highest levels since October 2024, the persistence and breadth of rising price pressures will warrant close monitoring.

JOLTS Job Openings (Previous: 6.93M, Forecast: 7.25M, Actual: 6.54M):

The number of job openings declined further to 6.5 million in December, according to the US Bureau of Labor Statistics, continuing the downward trend observed in recent months.

Over the same period, both hires and total separations were broadly unchanged at 5.3 million. Within total separations, quits remained steady at 3.2 million, while layoffs and discharges were little changed at 1.8 million.

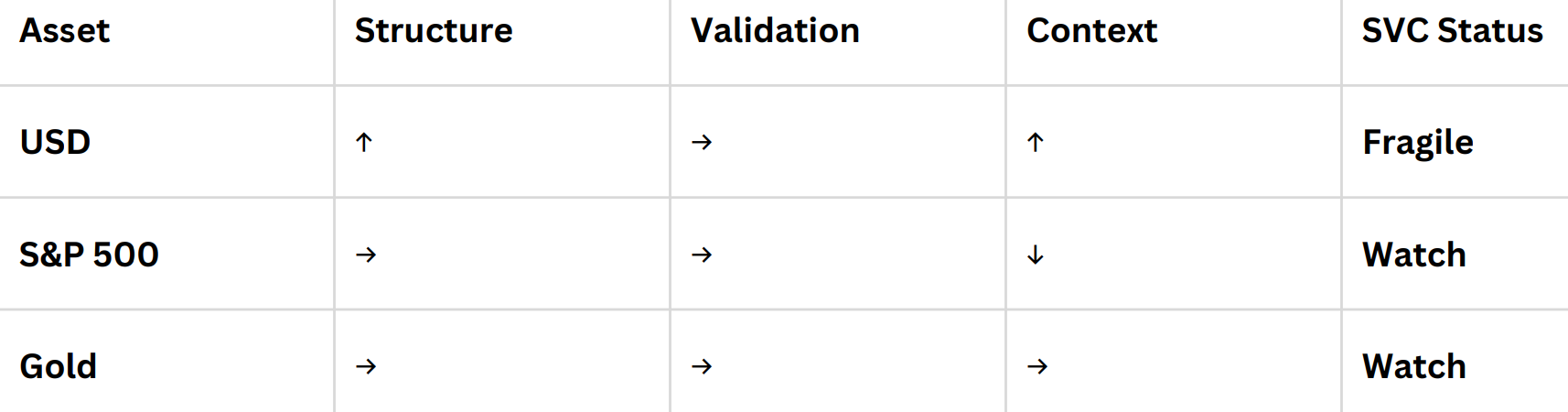

SVC Breakdown

USD

Since the announcement involving Kevin Warsh, the USD has continued to stabilise and has gained additional support from dollar-bullish developments over the course of the week.

The labour-market data that were postponed due to the government shutdown are expected to be released next week. Once those figures are available, we should be able to further validate and refine our SVC framework from a medium- to longer-term perspective.

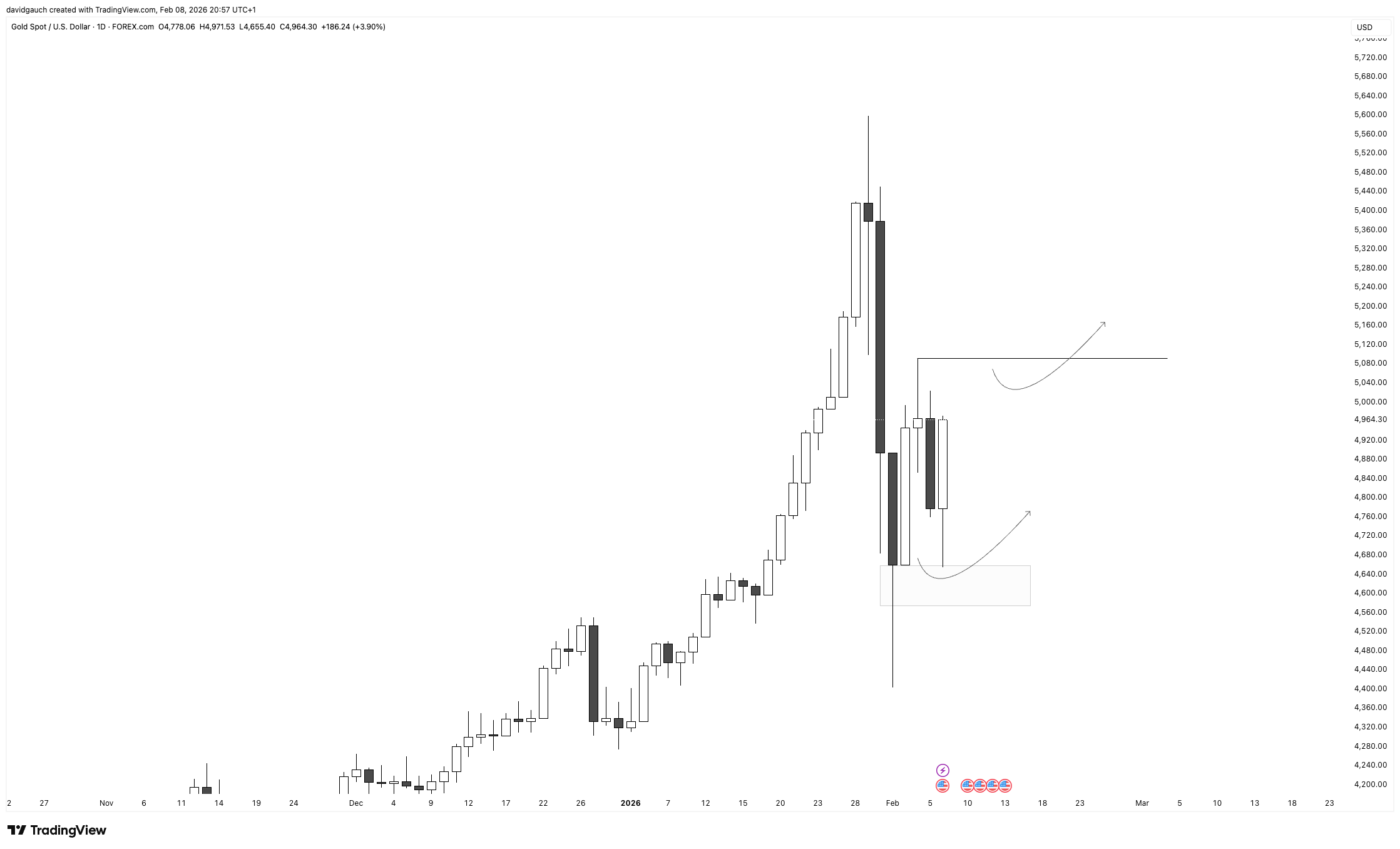

Gold

Price action in this area remained largely unchanged over the past week, broadly in line with the expectations outlined in our SVC framework. Rather than pursuing premature entries, we continue to focus on incoming macro data and market price action. There is no need to be first into a trade when the broader picture has yet to confirm.

US500

The earnings backdrop remains broadly constructive. While two additional mega-cap names, Alphabet (-3.9%) and Amazon (-11.7%), sold off following their results, largely due to continued increases in AI-related capital expenditures weighing on margins and near-term profitability, the overall picture at the index level remains solid. Aggregate earnings growth for the current season is tracking at approximately 13.0%.

At present, the market continues to trade between the two primary GEX zones. A break below the put-support area would open the door to further downside, whereas a decisive move through the gamma wall would point to additional upside potential.

Upcoming News

Retail Sales m/m

NFP

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research