SVC-Update

Weekly Recap & Outlook

Overview

No financial advice.

Last Sunday, the Federal Reserve released a statement by Jerome Powell indicating that the Department of Justice has issued a subpoena to appear before a grand jury, reportedly threatening criminal charges related to his testimony before the Senate Banking Committee last June. The testimony in question concerned, among other things, a multi-year renovation project of the Federal Reserve’s historic headquarters building. The initial market reaction was sharp: the US dollar sold off aggressively, as investors questioned the independence of the Federal Reserve amid concerns over a potential removal of the Fed Chair. This uncertainty pushed long-term yields sharply higher. However, having seen similar episodes in the past, it quickly became clear that this was a short-lived shock, with markets stabilizing and recovering shortly thereafter.

In addition, we received several important data releases this week, which I will break down below:

Consumer Price Index CPI y/y (Previous: 2.7%, Forecast: 2.7%, Actual: 2.7%):

US inflation held steady at 2.7% in December, unchanged from November and in line with expectations. Energy inflation eased, driven by falling gasoline prices and slower fuel oil increases, although natural gas prices rose further. Used car prices also cooled noticeably. In contrast, food and shelter inflation accelerated, with shelter remaining the largest monthly driver. Core inflation stayed at 2.6%, the lowest level since 2021 and below expectations. On a monthly basis, CPI rose 0.3%, while core CPI increased just 0.2%, undershooting forecasts.

Producer Price Index PPI y/y (Previous: 2.8%, Forecast: 3.0%, Actual: 3.0%):

US producer prices rose 0.2% m/m in November, lifting PPI inflation to 3.0% y/y. Core PPI (excluding food and energy) was flat on the month, but the annual core rate firmed to 3.0%. The report suggests businesses are absorbing higher costs, partly linked to tariffs, as trade service margins fell 0.8% in both October and November. Weaker labor market conditions and slower wage growth have limited firms’ ability to pass costs on. However, underlying inflation pressures remain strong: PPI excluding food, energy, and trade services rose again in November, pushing the annual rate to 3.5%, the highest level in eight months.

Retail Sales m/m (Previous: -0.1%, Forecast: 0.5%, Actual: 0.6%):

US retail sales rose 0.6% m/m in November, the strongest increase since July, rebounding from October’s decline and beating expectations. The gain was driven by a rebound in auto sales and strong holiday demand. Most categories posted increases, led by sporting goods and book stores, miscellaneous retailers, gasoline stations, building materials, and clothing. Sales were flat at general merchandise and electronics stores, while furniture sales dipped slightly. The control group, which feeds into GDP calculations, rose 0.4%, pointing to solid underlying consumer demand.

SVC Breakdown

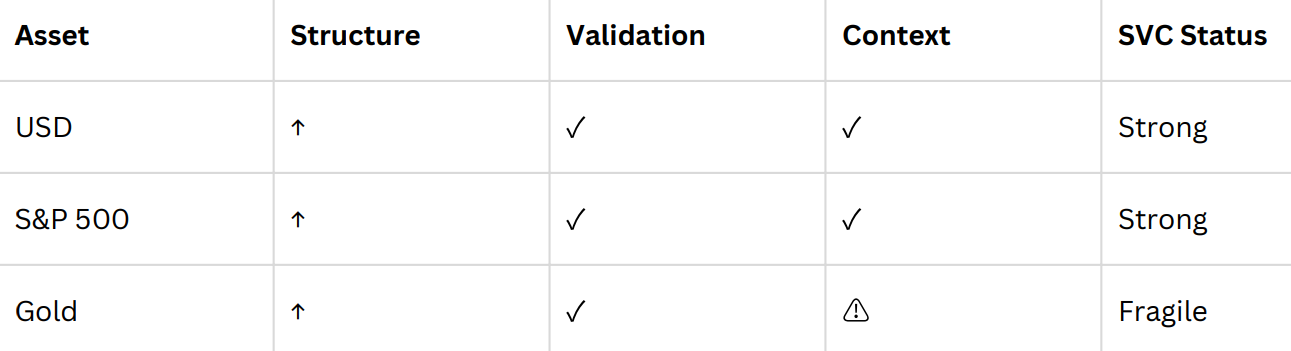

USD

Despite the initial shock on Sunday, the US dollar managed to stabilize and continued its move toward the 100 level. Equally noteworthy was the market’s reaction to the inflation data: despite slightly cooling inflation, which would typically weigh on the dollar, the initial bearish move was quickly bought, allowing the dollar to extend its bullish momentum.

The zone highlighted in our last SVC update worked very well, providing attractive entry opportunities:

Gameplan:

Gold

As expected, gold rallied strongly following the shock surrounding the subpoena of Jerome Powell, allowing the broader bullish trend to extend further. Readers who acted on our initial gold long ideas have been able to add further gains.

Gameplan:

US500

Earnings releases so far this week have been generally solid, not outstanding, but certainly not weak. Within the current SVC framework, the market remains strong, with fundamentals and trends intact.

The zones from the last update were also used effectively: the first experienced a slightly deeper drawdown, while the second aligned with put support, provided a clean and attractive entry.

Upcoming News

Core PCE Price Index

Final GDP

Flash PMI’s

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research

What stood out to me was how quickly markets distinguished noise from signal.

The initial shock tested confidence, but price action ultimately reinforced that macro trends and positioning still dominate headlines.

It’s a good reminder that volatility often reveals structure rather than breaks it. This captures the nuance most people miss.