SVC-Update

Weekly Recap & Outlook

No financial advice.

Alongside additional fundamental headlines, last week remained heavily shaped by geopolitical and fiscal uncertainty.

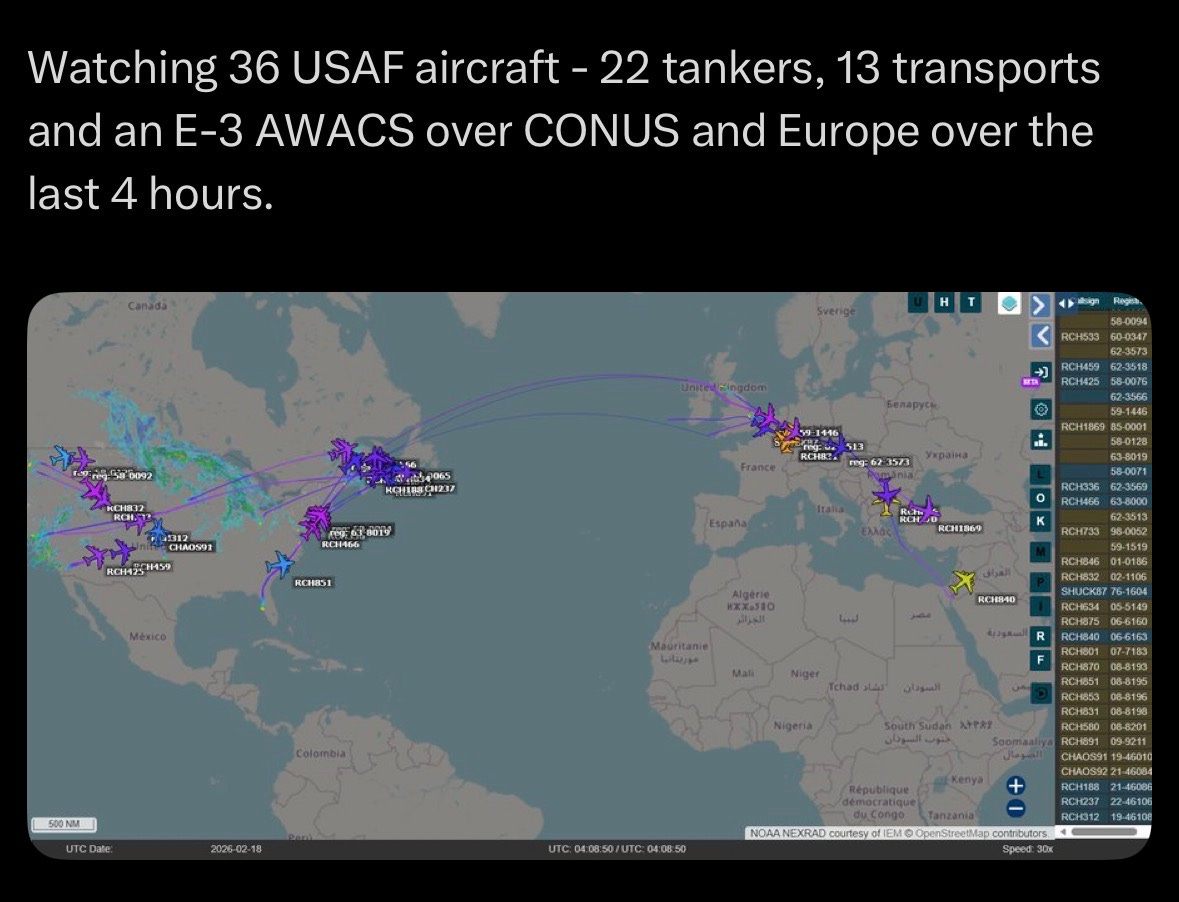

The United States deployed further military assets toward Europe, clearly signaling pressure toward Iran. President Donald Trump also emphasized that further escalations remain possible, even hinting at the prospect of a “limited strike.” Over the next 48 hours, Iran is expected to engage in negotiations in order to prevent a broader escalation.

However, the key headline on Friday afternoon was the ruling by the US Supreme Court, which declared the legal foundation of most tariffs insufficient. At the same time, the judges indirectly outlined alternative legal pathways through which these tariffs could potentially be reinstated, albeit with additional procedural effort.

In an initial step, President Trump announced the flat 10% tariff on all countries worldwide, which has now been increased to 15% for approximately the next five months under Section 122 of the Trade Act. Subsequently, formal investigations will be launched to create the legal basis for longer-term or permanent tariffs, for example under Section 301. In practical terms, the broader direction may not change significantly.

What could ultimately prove constructive for markets is the fact that a considerable amount of the currently restrictive dealer gamma expired on Friday. This may allow price action to move more freely without the countercyclical hedging flows from options market makers, potentially opening the door for a sustained break above 7,000 in the S&P 500.

A potential catalyst could arrive as early as Wednesday after the close, when the current earnings season unofficially concludes with the report from NVIDIA.

News Recap

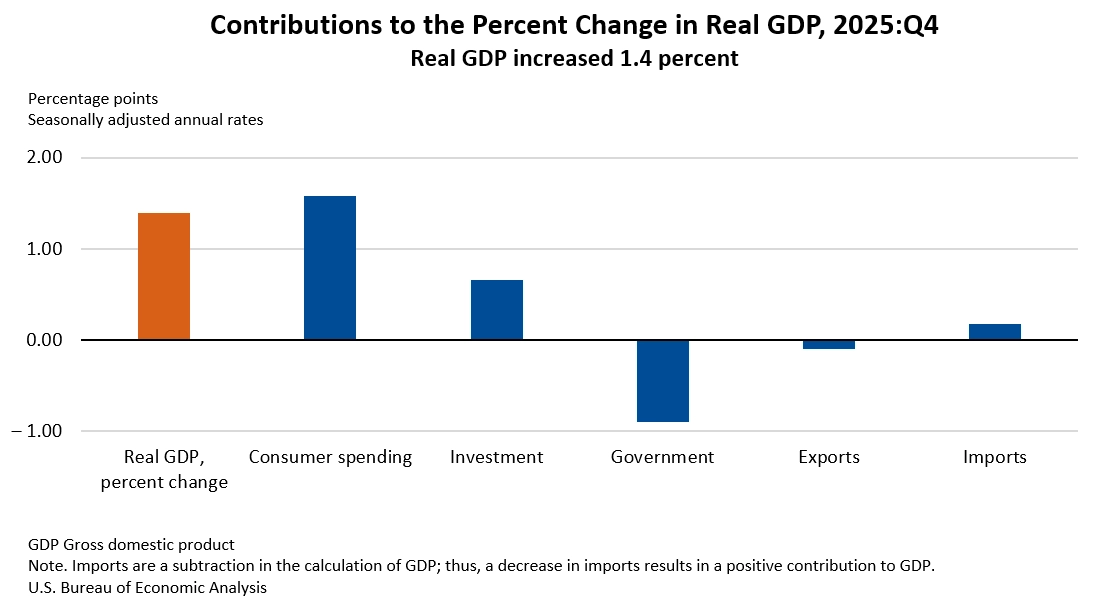

Advance GDP q/q (Previous: 4.4%, Forecast: 2.8%, Actual: 1.4%):

The US economy expanded at an annualized rate of 1.4% in Q4 2025, the weakest pace since Q1 2025, following 4.4% growth in Q3 and well below expectations of 3%. Consumer spending moderated (2.4% vs. 3.5%), weighed down by a slight contraction in goods consumption (-0.1%), while services spending rose 3.4%.

Exports declined by 0.9% after surging 9.6% in Q3, and imports also decreased, though at a slower rate (-1.3% vs. -4.4%). Government spending and investment contracted sharply by 5.1% (vs. +2.2%), subtracting 0.9 percentage points from overall growth due to the government shutdown.

On the positive side, fixed investment accelerated (2.6% vs. 0.8%), driven by strong gains in intellectual property products (7.4%) and equipment (3.2%), while the contraction in structures eased (-2.4% vs. -5.0%). The decline in residential investment also moderated (-1.5% vs. -7.1%).

For the full year 2025, the US economy expanded by 2.2%, down from 2.8% in 2024.

Core PCE Price Index m/m (Previous: 0.2%, Forecast: 0.3%, Actual: 0.4%):

The core PCE price index, the Federal Reserve’s preferred inflation gauge, rose 0.4% month-over-month in December 2025, exceeding expectations of 0.3%. This marked the strongest monthly increase since February and reinforces the FOMC’s message that disinflation is progressing more slowly than anticipated.

On a yearly basis, core PCE increased by 3%.

United States Flash Services PMI (Previous: 52.7, Forecast: 53.0, Actual: 52.3)

The S&P Global US Services PMI declined to 52.3 in February 2026 from 52.7 previously, missing expectations and marking the slowest expansion in ten months.

New business inflows softened, particularly due to weaker export demand. Slower client momentum led firms to reduce the pace of hiring. At the same time, service providers raised selling prices to a seven-month high, while input cost inflation remained elevated, albeit below recent peaks.

Looking ahead, companies remain optimistic that improving weather conditions, lower interest rates, and potential tax relief could support activity over the coming year.

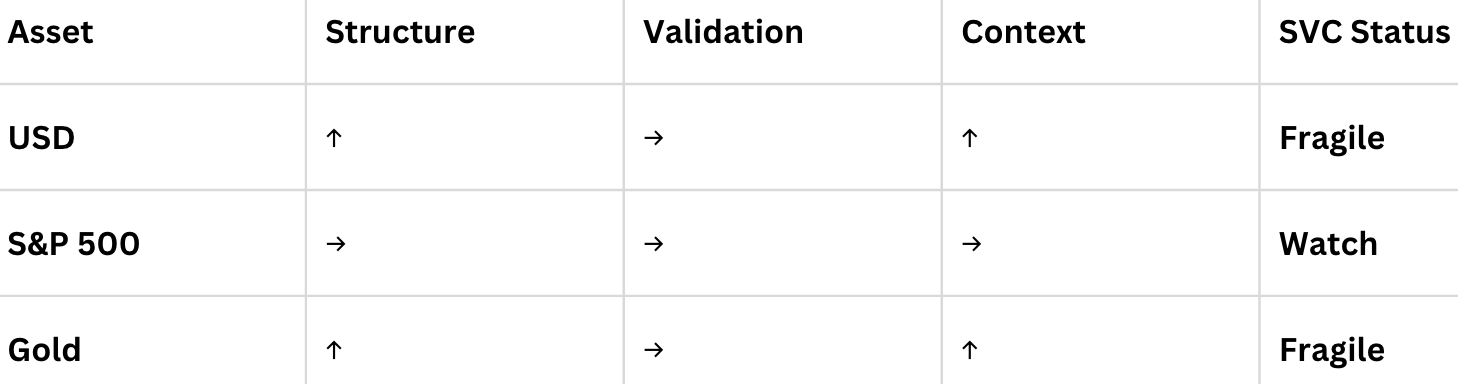

SVC Breakdown

USD

The Dollar continued its move toward our first target zone last week, congratulations to those who captured the long from the previous area.

Fundamentally, the data paints a mixed picture: sticky inflation, slowing GDP, and softer PMIs on one side. On the other, a still-resilient labor market and ongoing geopolitical tensions could provide near-term support for the Dollar.

At this stage, there does not appear to be a strong enough catalyst to reverse the prevailing direction, yet positioning also suggests the market is not fully committed to an aggressive long bias either.

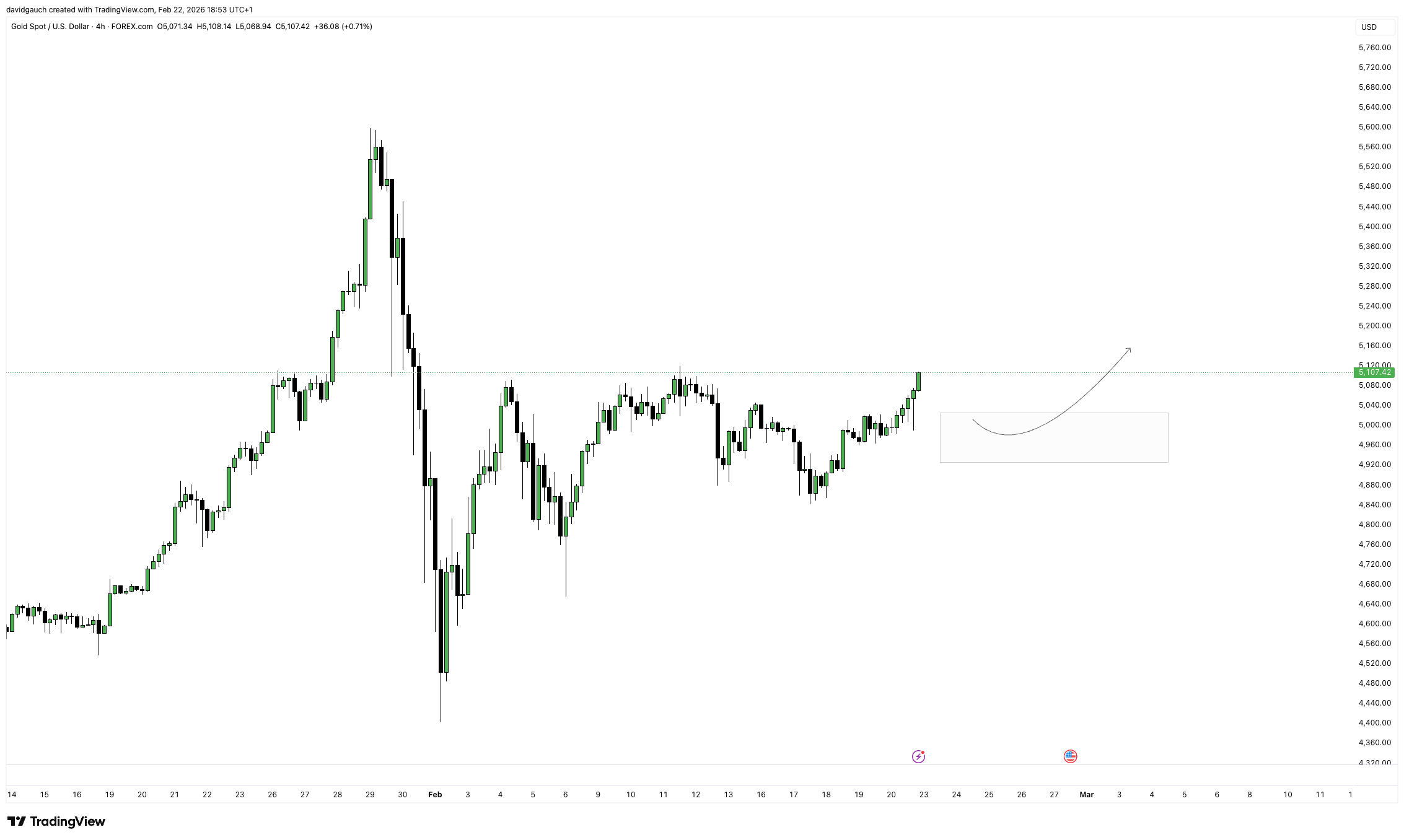

Gold

While Gold is partially influenced by Dollar strength, the current geopolitical backdrop continues to justify a constructive long bias.

I was able to capture a strong Gold long this week, which has so far developed into a 1:22 risk-reward profile.

S&P 500

The US500 regained some ground on Friday following the news that Trump’s tariffs were deemed legally insufficient. Technically, the index traded within the same range throughout the week, largely influenced by dealer gamma hedging flows.

With a significant portion of options expiring recently, dealers now have more flexibility. Should we receive one or two bullish catalysts, a sustained move above the 7,000 level in the S&P 500 could materialize more easily.

Upcoming News

NVDA Earnings

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research