SVC-Update

Weekly Recap & Outlook

If you haven’t joined my free Telegram channel yet, you can get daily market insights, news updates, and my personal ideas. Click the link below to join and stay updated:

No financial advice.

With markets becoming increasingly complex and headlines often sending mixed signals, this update aims to simplify the key macro drivers behind current pricing and outline what could matter going forward.

Current market conditions continue to be driven by a combination of geopolitical risk, tightening financial conditions, and shifting policy expectations.

The ongoing war remains a key overhang, sustaining elevated uncertainty and limiting risk appetite across global markets. At the same time, oil prices continue to trend higher, reinforcing inflationary pressures and complicating the macro outlook.

Interestingly, gold has been selling off despite the uncertain backdrop, highlighting that markets are not positioning for a traditional risk-off environment, but rather reacting to rising real yields and tighter liquidity conditions.

Equities have come under pressure, and the current sell-off appears fundamentally justified. The combination of higher yields, a persistently strong dollar, and a Federal Reserve maintaining a hawkish hold is creating a challenging environment for risk assets. Financial conditions continue to tighten, forcing a repricing across equity markets.

On the policy side, expectations have shifted materially. Markets are no longer pricing in rate cuts for this year and have started to incorporate the possibility of additional hikes. This reflects both the persistence of inflation and the Fed’s commitment to maintaining restrictive policy for longer.

At the same time, stagflation risks are rising. Growth and labour market dynamics are showing signs of moderation, while inflation remains elevated, partly reinforced by higher energy prices. This combination increases uncertainty and limits the range of favorable macro outcomes in the near term.

However, it is important to note that the current pricing of further rate hikes may be somewhat premature. Market sentiment appears increasingly anxious, with positioning reflecting a more defensive and reactive stance.

This creates an asymmetric setup. In the event of positive developments, particularly on the geopolitical front, the potential for a sharp, V-shaped recovery remains elevated. Such dynamics are typical in environments where sentiment is fragile and positioning is skewed.

As always, markets tend to overshoot in both directions. While the current environment justifies caution, it also creates the foundation for selective opportunities.

News Recap

US PPI m/m (Previous: 0.5%, Forecast: 0.3%, Actual: 0.7%):

US producer prices increased by 0.7% month-over-month in February, accelerating from 0.5% in January and coming in well above expectations of 0.3%. This marks the strongest monthly increase in seven months and adds to evidence that upstream inflation pressures remain persistent.

The move was largely driven by goods prices, which rose 1.1%, the biggest increase since August 2023. A significant contributor was a sharp surge in food-related components, particularly a 48.9% increase in fresh and dry vegetable prices. Energy-related categories, including diesel fuel, gasoline, and jet fuel, also moved higher, reinforcing the inflationary impulse.

On the services side, prices rose by 0.5%, moderating from the previous month but still contributing to overall inflation. Notably, traveler accommodation services saw a strong increase, providing the largest upside contribution within services.

Core PPI rose 0.5%, easing from January’s 0.8% but still exceeding expectations. On a year-over-year basis, headline PPI accelerated to 3.4%, the highest level in a year, while core PPI climbed to 3.9%. Overall, the data points to continued inflation persistence at the producer level, with potential implications for future consumer price dynamics.

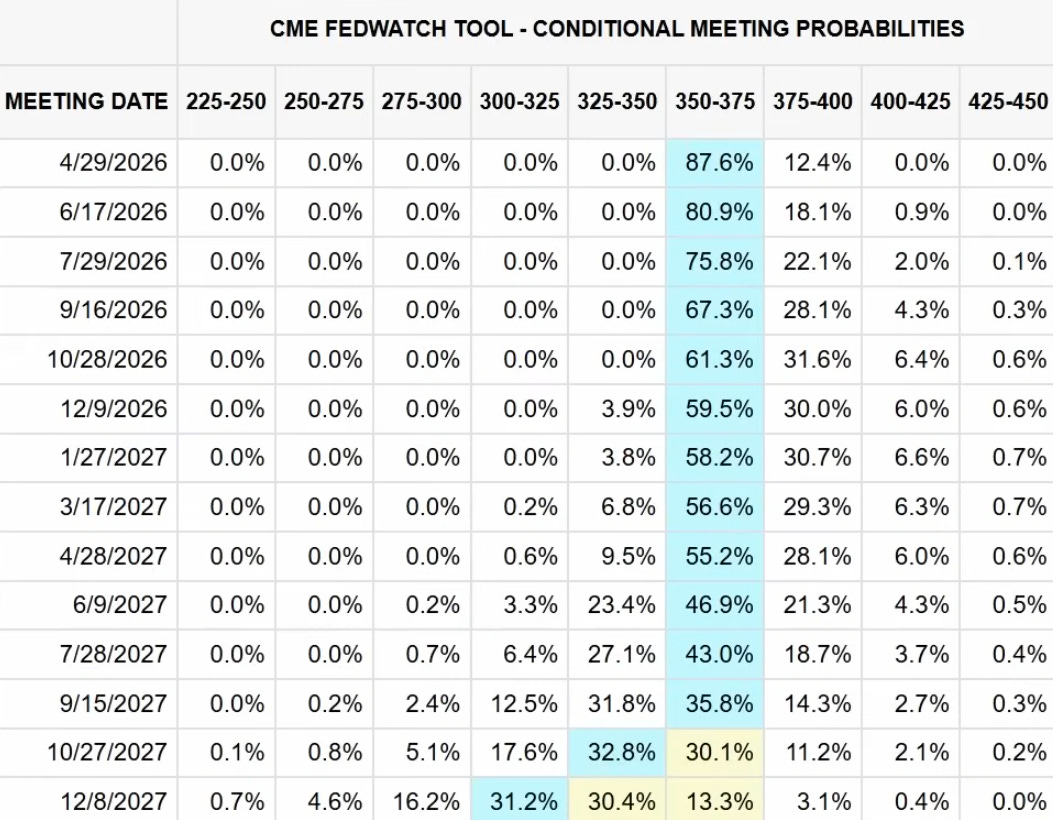

Federal Funds Rate (Previous: 3.75%, Forecast: 3.75%, Actual: 3.75%):

The Federal Reserve left the federal funds rate unchanged at a target range of 3.50%–3.75% for a second consecutive meeting, in line with market expectations.

While policymakers continue to describe economic activity as solid, the broader message remains cautious. Labour market conditions are showing signs of moderation, and inflation, although off its peaks, remains somewhat elevated. Additionally, geopolitical developments, particularly the ongoing conflict involving Iran, were highlighted as a source of uncertainty.

Updated projections reflect a slightly stronger growth outlook, with GDP forecasts revised modestly higher for both 2026 and 2027. At the same time, inflation expectations have been revised upward. Both headline and core PCE are now expected to reach 2.7% in 2026, with further upward revisions for 2027.

Taken together, the Fed’s stance can be characterized as a “hawkish hold”: policy remains restrictive, inflation risks are still skewed to the upside, and any easing cycle is likely to be gradual and conditional on clearer disinflationary progress.

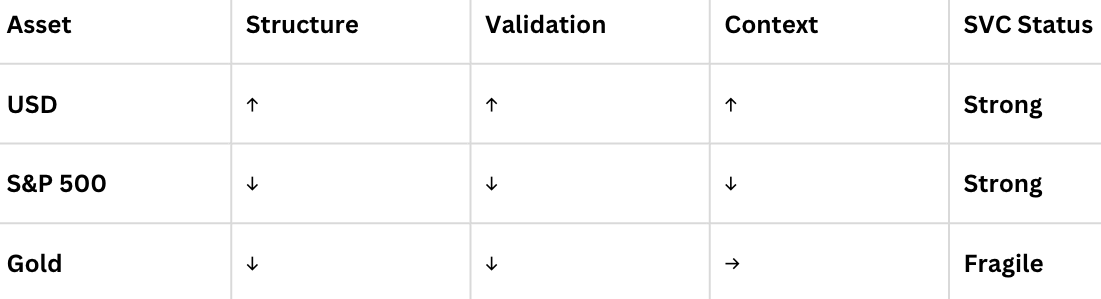

SVC Breakdown

USD

With no resolution yet in sight in the Middle East, the focus remains on USD strength. The combination of rising real yields in the US and the dollar’s traditional role as a risk-off asset continues to support further upside potential.

Gold

Our previously highlighted support area failed to hold, and with ongoing uncertainty alongside weaker demand for gold, prices could be pushed below the 4400 level. That said, a potential upside correction from this area remains possible, offering selective opportunities for short-term buyers.

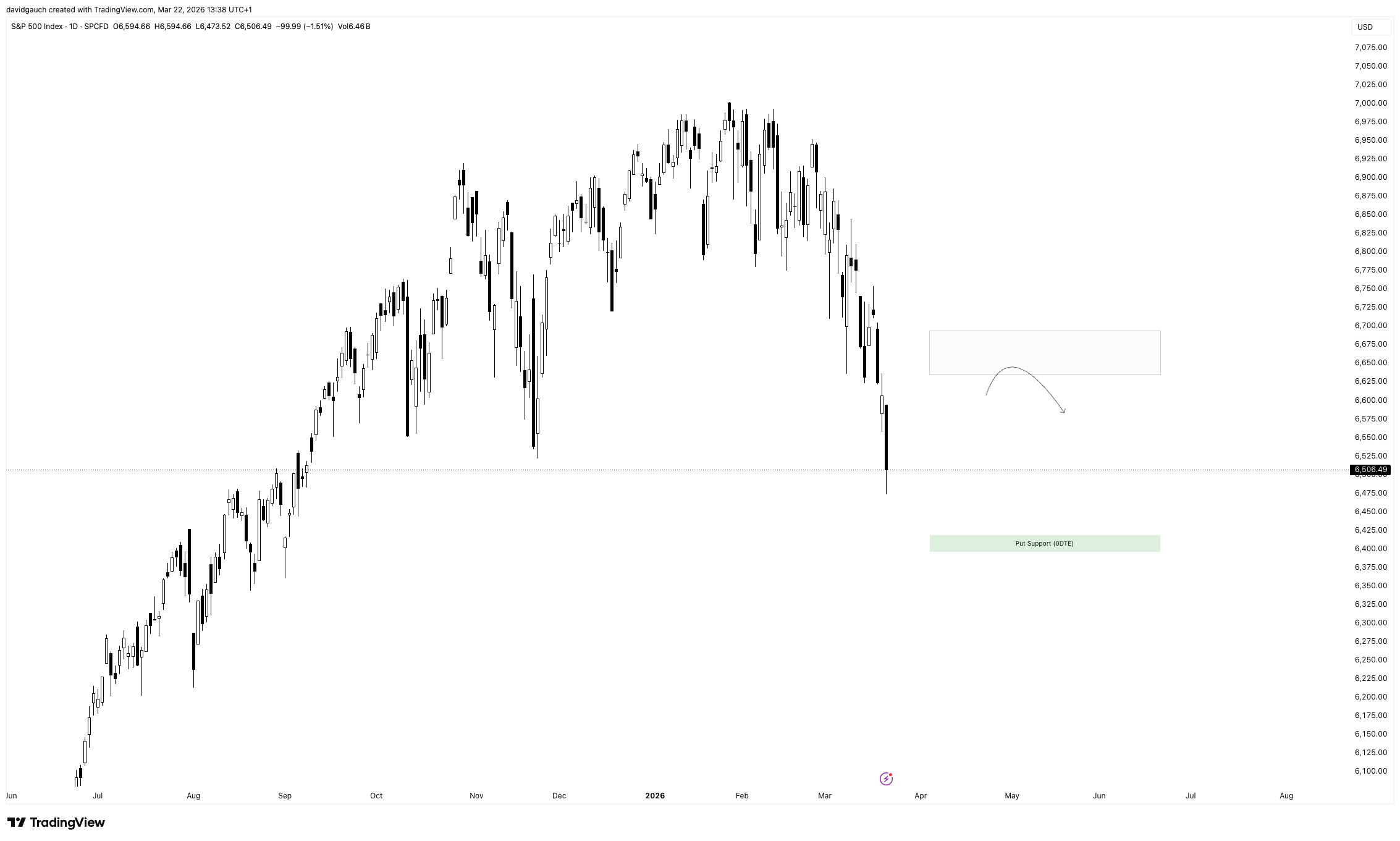

S&P 500

As noted over the past weeks, the previous gamma put support level failed to hold, turning from a stabilizing factor into an area for further downside. At present, there are no major gamma levels providing meaningful support for the SPX.

This leaves market direction largely dependent on developments in the Middle East. Without a de-escalation, downside pressure is likely to continue, with potential targets toward the 6400 level.

Upcoming News

Flash PMI’s

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research