SVC-Update

Weekly Recap & Outlook

No financial advice.

Overall, the week was relatively calm with very limited market-moving fundamental data (aside from PPI). As discussed in previous updates, the main focus remained on the situation in Iran, which escalated significantly over the weekend. Below is a structured overview of what happened and how markets may react going forward.

A major escalation in the Middle East began on 28 Feb 2026 when the United States and Israel launched coordinated airstrikes inside Iran, targeting regime and military infrastructure. The operation, widely reported as one of the most significant joint strikes in recent decades, reportedly killed top Iranian leadership including Supreme Leader Ayatollah Khamenei, triggering a sharp regional military response.

In immediate retaliation, Iran’s Islamic Revolutionary Guard Corps (IRGC) declared all U.S. and Israeli military assets across the region legitimate targets and launched waves of missile and drone strikes. These strikes have spread far beyond direct Iran-Israel theaters and hit multiple Gulf states:

United Arab Emirates: Infrastructure and Airports in Dubai and Abu Dhabi were damaged and flights suspended, at least a few civilian casualties were reported, with debris strikes and fires in major hubs.

Kuwait City: Kuwait International Airport sustained damage from incoming drones.

Bahrain: U.S. Fifth Fleet facilities and surrounding areas have been hit.

Oman: Ports and an oil tanker were struck, marking a widening of the conflict footprint.

Doha (Qatar) and other Gulf capitals also reported missile interceptions and fallout effects.

The broad geographic spread underscores that this is no longer a bilateral confrontation. Iran’s retaliation now impacts Gulf Arab states long considered relatively stable or neutral.

On the diplomatic front, the UN Security Council convened an emergency session, with global powers calling for de-escalation and opposing both the initial strikes and Iran’s retaliation.

Closure of the Strait of Hormuz

The Strait of Hormuz remains the most critical oil transit chokepoint globally. Roughly 20% of worldwide oil consumption and a significant share of LNG exports pass through this narrow corridor between Iran and Oman. A disruption could have immediate global consequences.

Export Destinations

The majority of crude oil transiting Hormuz flows to Asia. China, India, Japan, and South Korea account for the largest share of imports. These economies are structurally more exposed to supply interruptions than the US or Europe.

Dependencies

China and India rely heavily on Gulf producers such as Saudi Arabia, Iraq, UAE, and Kuwait.

Japan and South Korea import the majority of their crude from the Middle East.

Europe has diversified supply sources but would still face price transmission effects.

The United States has limited direct dependence but would experience higher energy prices due to global pricing dynamics.

LNG Risk

Qatar’s LNG exports also transit Hormuz. Any disruption would likely tighten Asian gas markets and increase volatility in global LNG pricing.

Expected Market Gaps at Open

USOIL +11.89%

GOLD +2.49%

SILVER+3.94%

EURUSD -0.36%

DOW 48440 -0.86%

NASDAQ -0.92%

News Recap

PPI m/m (Previous: 0.4%, Forecast: 0.3%, Actual: 0.5%):

The U.S. Bureau of Labor Statistics reported that the Producer Price Index for final demand rose 0.5 percent in January, seasonally adjusted. This follows a 0.4 percent increase in December 2025 and a 0.2 percent rise in November. Unadjusted, the index climbed 2.9 percent over the 12 months ending January 2026. January’s gain was driven by a 0.8 percent rise in prices for final demand services, while prices for final demand goods fell 0.3 percent. Excluding food, energy, and trade services, the index increased 0.3 percent in January, marking the ninth straight monthly rise, and was up 3.4 percent over the past year.

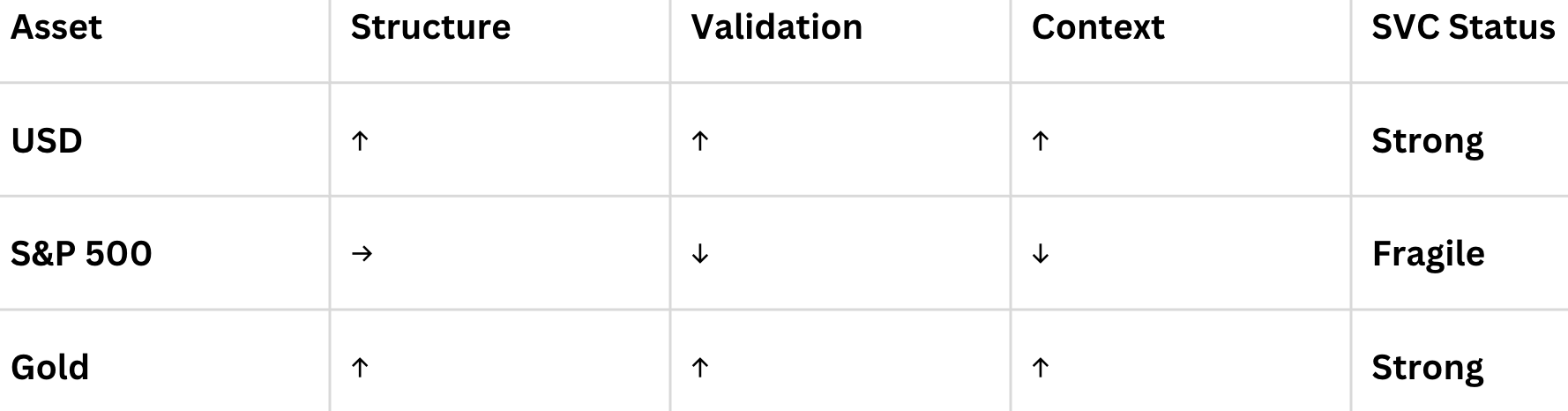

SVC Breakdown

USD

The zone identified in the last SVC update provided additional solid long entries. Given the current geopolitical escalation, the U.S. dollar should continue to benefit from safe haven flows, potentially pushing price action toward our next target zone.

Gold

The previously mentioned area was not filled. However, the broader direction remains clear: upside. If the conflict continues to escalate or prolong, gold could extend toward the next major upside targets around 6000.

S&P 500

Under the current risk-off environment, equities remain vulnerable to geopolitical shocks. A medium-term bearish scenario becomes increasingly plausible if the 6800 level is decisively broken to the downside.

Market sentiment can also be observed in recent NVIDIA earnings. Despite delivering a strong beat, the stock declined roughly 5% the following day, not a constructive bullish signal.

Upcoming News

ISM PMI’s

NFP

Retail Sales

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research