SVC-Update

Weekly Recap & Outlook

Before we begin, I want to make it clear that there are multiple social media accounts impersonating me. I will never contact you directly or attempt to sell any services. This is my only official account.

No financial advice.

Welcome back to another edition of our SVC Update.

Since our last update, both the technical and fundamental landscape had remained largely unchanged until last Friday. The release of the latest Non-Farm Payrolls (NFP) report triggered significant moves across multiple asset classes and provided markets with fresh direction.

NFP Recap:

The U.S. economy added 172K jobs in May 2026, significantly exceeding market expectations of 85K, following an upwardly revised gain of 179K in the previous month. The report continues to highlight the resilience of the U.S. labor market.

Job growth was primarily driven by Leisure and Hospitality (+70K), led by Food Services and Drinking Places (+48K), Local Government (+55K), Healthcare (+35K), and Manufacturing (+7K).

On the other hand, employment within Financial Activities declined by 22K, mainly due to weakness in Insurance Carriers and Related Activities (-11K) and Commercial Banking (-3K).

Meanwhile, Transportation and Warehousing remained largely unchanged (+1K), while sectors such as Construction, Wholesale Trade, Retail Trade, Information, and Professional & Business Services showed little movement.

Additionally, upward revisions to previous months added further strength to the report, with March and April payrolls now estimated to be 93K higher than previously reported.

These figures align closely with the thesis outlined in our previous update, where we anticipated further upside potential for the U.S. Dollar. More importantly, they reinforce the Federal Reserve’s current policy stance: Higher for longer.

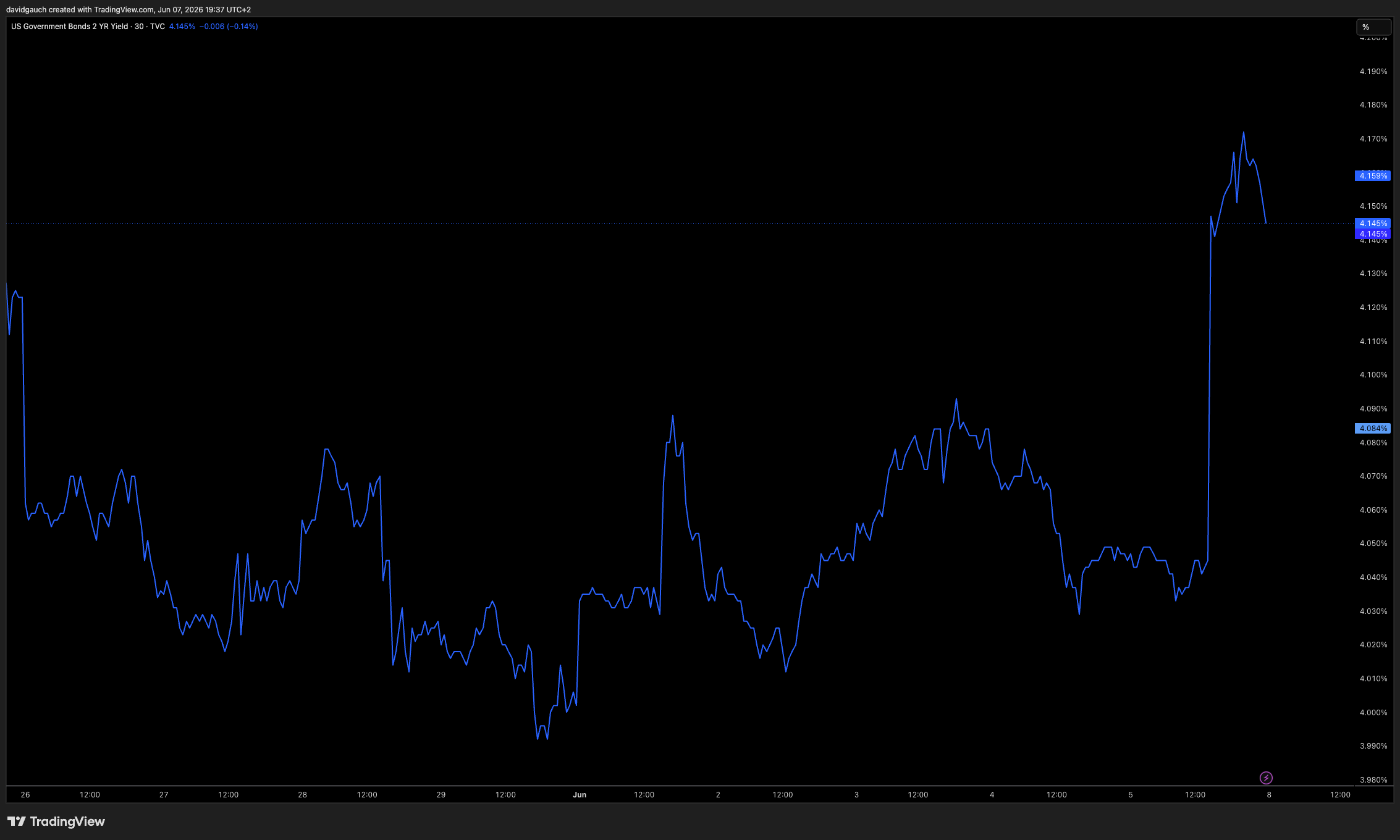

The immediate market reaction was visible in the U.S. 2-Year Treasury Yield, which climbed to 4.145% following the release, reflecting a reassessment of future monetary policy expectations.

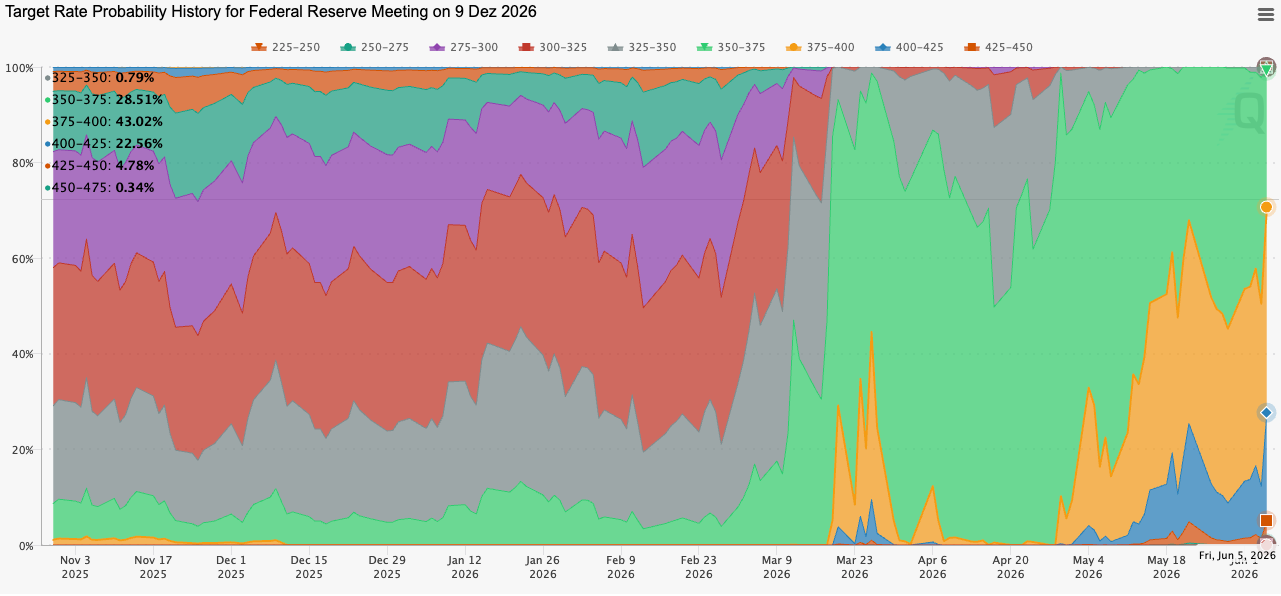

Looking at the current Fed target rate probabilities, markets now assign a 43% probability of one additional rate hike and 22% of two hikes this year, replacing earlier expectations that were centered around potential rate cuts or prolonged holds.

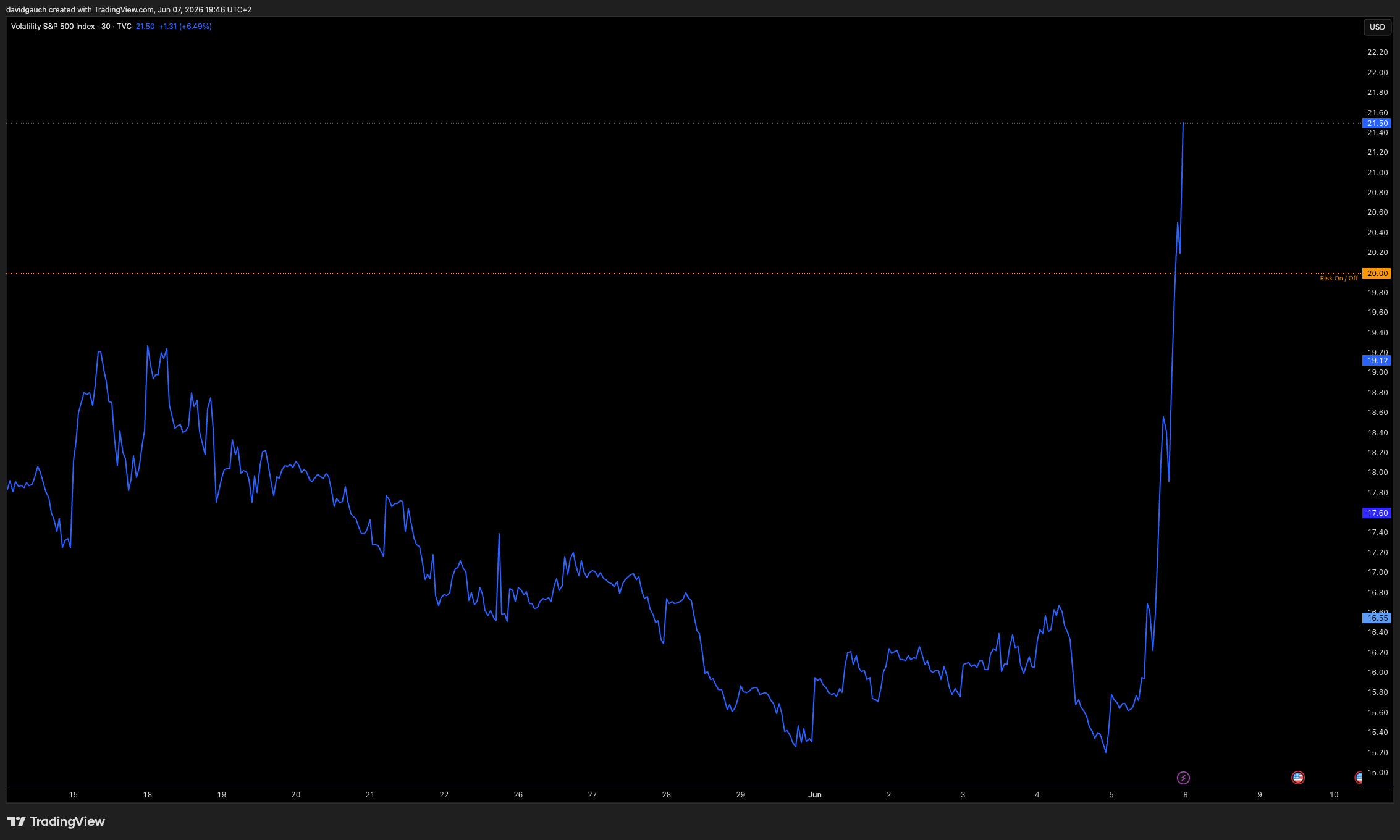

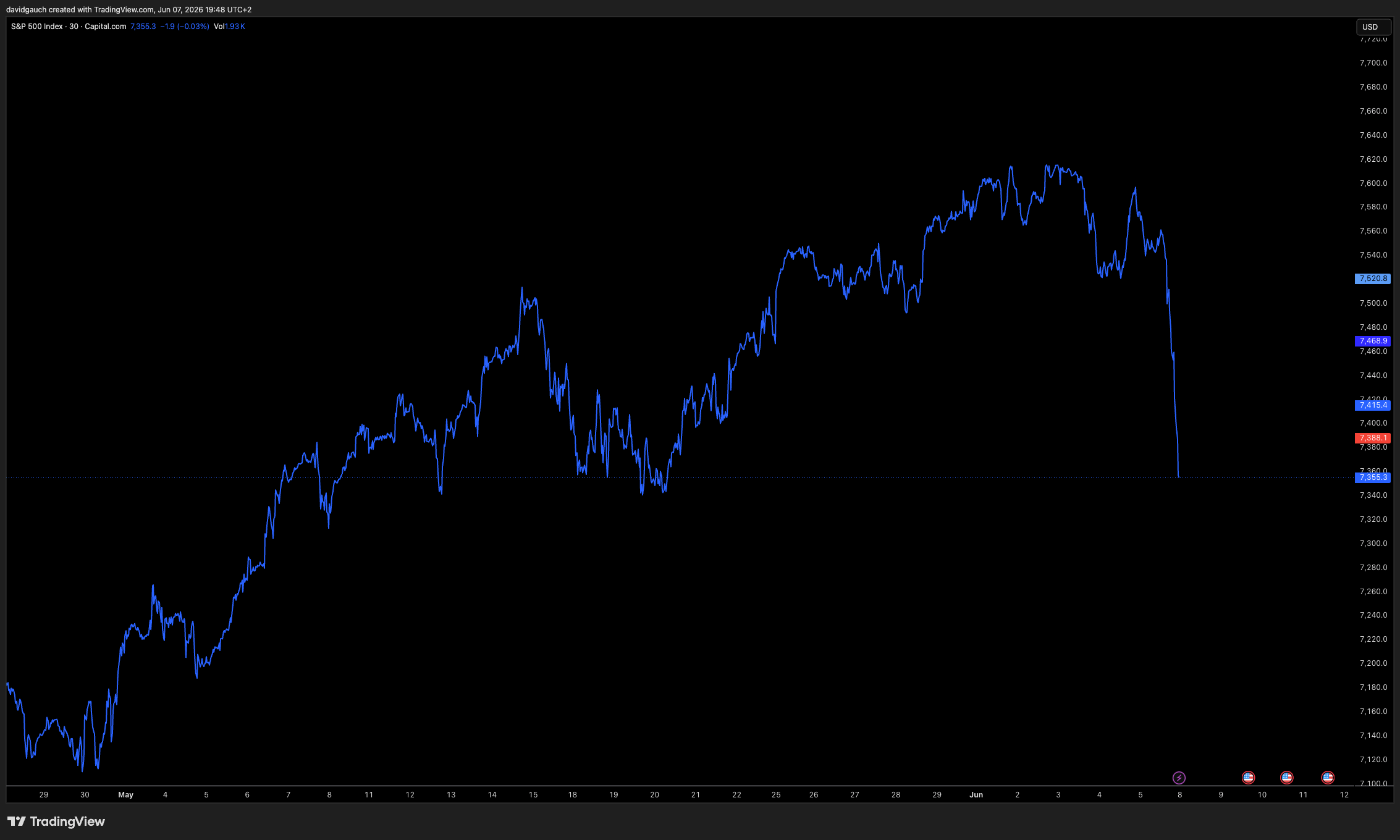

The impact of this repricing was also clearly visible in volatility markets. After an initial adjustment period, the VIX surged sharply and broke above the key 20 level, signaling a meaningful increase in risk aversion.

At the same time, an already stretched equities market became vulnerable to profit-taking and systematic CTA selling pressure. As a result, U.S. equities experienced a significant decline, with major indices falling nearly 3% on Friday.

The latest data provides a clearer framework for assessing the current macroeconomic environment:

The U.S. economy remains remarkably resilient, supported by moderate but positive GDP growth, continued expansionary PMI readings, and a strong labor market.

At the same time, inflationary pressures remain persistent. Rising energy prices, driven by the ongoing conflict involving Iran, are increasingly feeding into broader inflation dynamics through secondary-round effects.

As a result, the Federal Reserve, under the leadership of Kevin Warsh, currently has little justification for initiating rate cuts. If anything, the risk is gradually shifting in the opposite direction.

While the base case remains a hold at upcoming meetings, the probability of further tightening has increased materially. This development continues to provide fundamental support for the U.S. Dollar while potentially maintaining downward pressure on risk assets and equities.

ECB in Focus:

On the other side of the Atlantic, attention next week will shift to the European Central Bank.

The ECB is expected to raise rates at its upcoming meeting. However, this outcome has already been largely priced into markets.

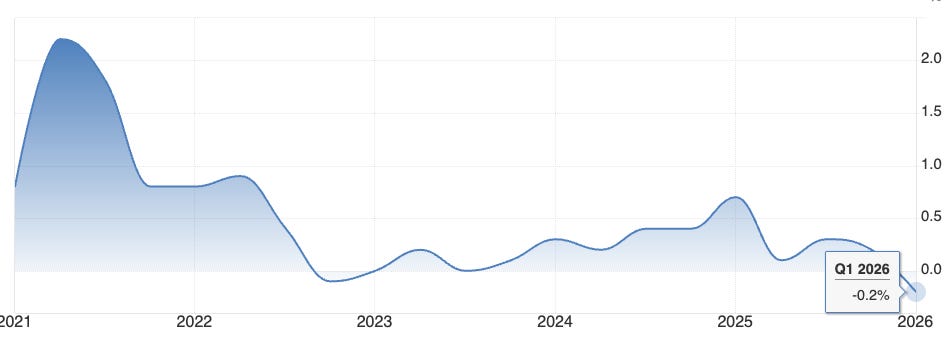

As a result, the Euro struggles to generate meaningful strength against the U.S. Dollar, particularly following last week’s disappointing GDP release, which came in at -0.2%.

Consequently, we maintain the same core macro theses outlined in our previous updates.

More details can be found in the Outlook section below.

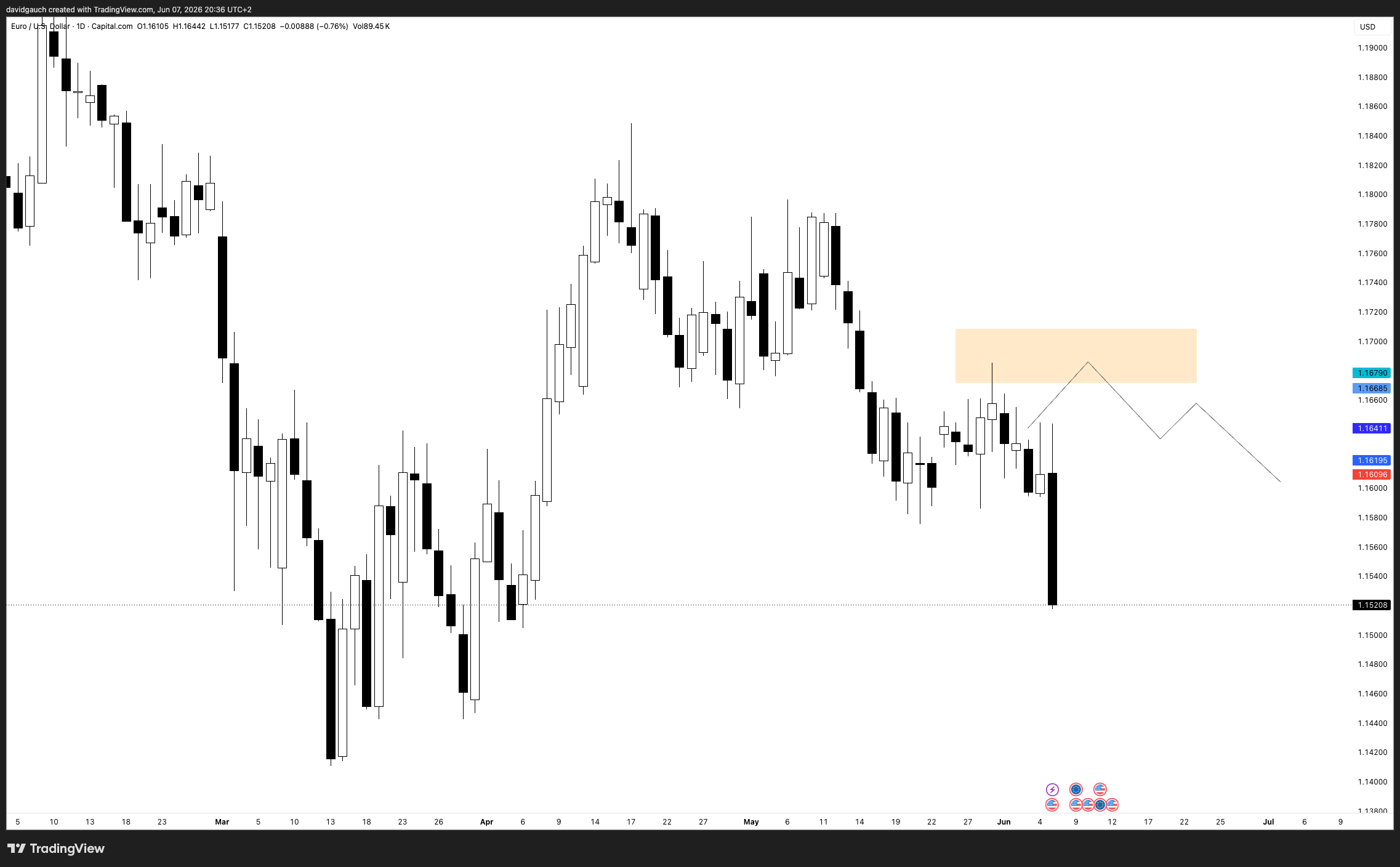

Our Premium Members were already able to anticipate this move in EURUSD ahead of the market.

Below is a screenshot from the analysis that was shared in our Premium Subscriber Chat:

How it played out:

Institutional Positioning

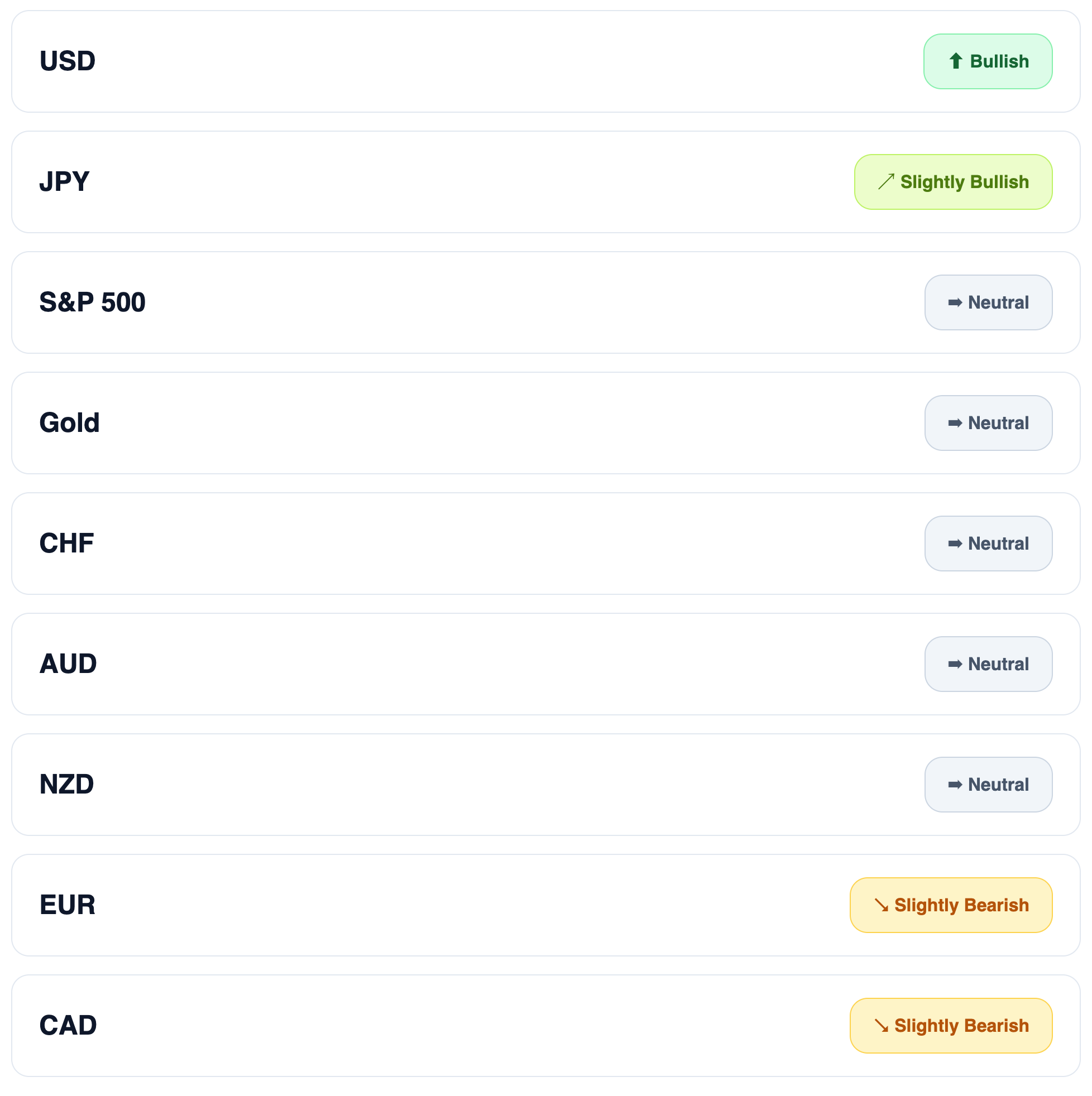

Before turning to this week’s outlook, below is an overview of recent positioning shifts across major asset classes, based on our proprietary Gauch Research COT Visualizer.

Outlook

Upcoming News

US CPI + PPI

BoC Overnight Rate

ECB Main Refinancing Rate

UK GDP

Wishing you a successful week ahead,

David Gauch - Founder, Gauch Research

very informative, thanks!