SVC-Update

Weekly Recap & Outlook

Once again: If you haven’t joined my free Telegram channel yet, you can get daily market insights, news updates, and my personal ideas. Click the link below to join and stay updated:

No financial advice.

Markets have been highly volatile over the past weeks following the escalation in the Middle East after the U.S. and Israel attacked Iran. What is becoming increasingly clear is that the market is starting to move away from the initial expectation of a quick resolution.

Major U.S. indices, including the Dow Jones, have now entered correction territory (more than -10% from recent highs), confirming that this is no longer a short-term reaction but a broader repricing of risk.

The key driver remains the energy market. Oil prices have surged significantly, with Brent crude moving above $110 (+55% in March), as the conflict directly impacts critical global supply chains. Iran’s control over the Strait of Hormuz is central here, affecting not only oil flows but also essential resources like fertilizers and helium. Even if the situation were to stabilize quickly, the damage to energy infrastructure suggests that prices are unlikely to return to previous levels anytime soon.

What is changing now is the market narrative. The idea of a short-lived conflict is fading, and markets are beginning to price in a prolonged period of elevated energy costs. This shift has clear implications: rising inflation pressures, reduced expectations for rate cuts, increasing bond yields, and a continued rise in volatility.

At the same time, existing macro risks, such as AI-related disruptions and concerns in private credit markets, are adding further pressure to the outlook.

In simple terms, the market is transitioning from hope to reality. A prolonged conflict with structurally higher energy prices implies higher inflation, rising yields, a stronger U.S. dollar, and continued downside pressure on equities.

News Recap

US Flash Services PMI (Previous: 51.7, Forecast: 52.0, Actual: 51.1):

The Services PMI declined to 51.1, marking the weakest expansion in nearly eleven months and missing expectations. Demand is clearly slowing, with both domestic and international orders losing momentum as uncertainty around the Middle East conflict and fiscal concerns weigh on confidence. Businesses are already reacting to this softer environment by reducing staff, pointing to early cracks in the labor market. At the same time, forward-looking expectations have deteriorated, reaching their lowest levels since October, highlighting a cautious outlook across the sector.

US Flash Manufacturing PMI (Previous: 51.6, Forecast: 51.5, Actual: 52.4):

The Manufacturing PMI rose to 52.4, beating expectations and signaling stronger activity. However, this strength is largely driven by precautionary behavior rather than genuine demand. Firms are increasing production and building inventories in anticipation of supply disruptions and rising prices linked to the ongoing conflict. While new orders improved and export demand stabilized, employment growth slowed and supply chain pressures intensified, with delivery times rising sharply. In addition, both input and output prices surged, reinforcing the inflationary environment despite the headline strength in the sector.

SVC Breakdown

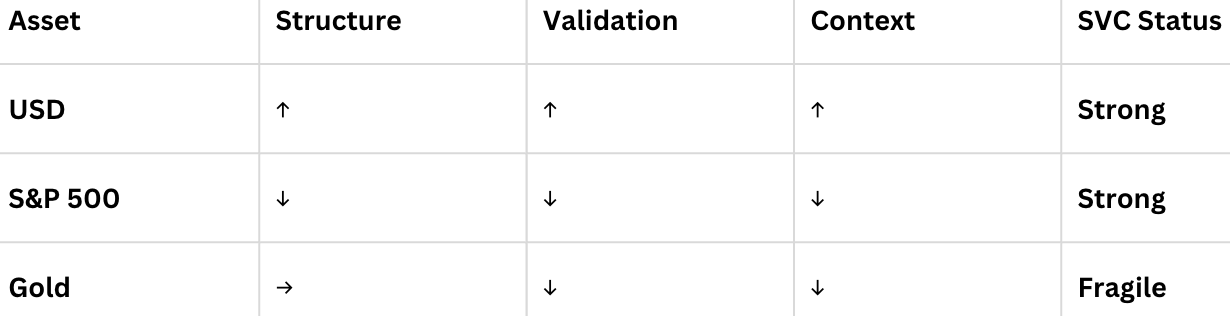

USD

Since the last update, nothing has changed regarding the broader outlook for the U.S. dollar. The overall game plan remains intact: pullbacks continue to present potential entry opportunities.

A good example was seen on March 23, when comments from Trump about possible peace negotiations triggered a temporary move lower. However, this was quickly dismissed after Iran labeled the statements as fake news, leading to a reversal. This dip provided a solid long opportunity, which was shared in the Telegram channel.

Gold

The downside target from the last update was reached last week, and we did see a reaction from that level.

From here, the focus shifts to the developing structure. A move back into the prior range appears realistic, but should be approached with reduced risk. The environment remains highly driven by external factors, so any positioning should stay flexible and well-managed.

S&P 500

As mentioned in the previous update, the downside continuation in the SPX was the highest probability scenario. The zone outlined in the last update provided very solid short entries, offering clean opportunities on the move lower.

For further downside continuation, the zone mentioned below could act as a key area for potential entries. Keep in mind that in the current environment, moves can remain volatile, so execution and risk management stay critical.

Gameplan:

Upcoming News

JOLTS

Retail Sales

NFP

Wishing you a successful trading week ahead,

David Gauch

Founder, Gauch Research