Alpha Bets - Part I

A Luxury Compounder in Disguise

Welcome to the first edition of Alpha Bets, a new series where we break down individual stocks and the investment story behind them.

Today we’re starting with a company almost everyone knows, not because of its financials, but because of what it represents.

Ferrari ($RACE) is often seen as just another automaker. But once you look at the numbers and the business model, it becomes clear:

This is not a car company.

It is a luxury brand that happens to sell cars.

The Core Model: Scarcity by Design

Ferrari’s strategy is simple:

Demand must always exceed supply.

The company deliberately limits production, even though it could sell more vehicles. The goal is not volume. The goal is value per client.

This controlled scarcity creates:

Long waiting lists

Strong pricing power

High resale values

Persistent exclusivity

Ferrari does not compete with Ford or Volkswagen.

Economically, it behaves far more like Hermès or LVMH.

Where the Money Really Comes From

Cars are the core product, but margins are driven by mix and customization.

A Ferrari is rarely sold “base spec.”

Clients add:

Custom paint finishes

Unique interiors

Performance upgrades

Bespoke elements

These options carry exceptionally high margins and significantly increase revenue per vehicle.

Beyond that, Ferrari benefits from:

High-margin after-sales services

Spare parts

Licensing and brand partnerships

Formula 1 exposure

The ecosystem reinforces the brand, and the brand reinforces pricing power.

Financial Profile: Luxury Economics

The numbers confirm the thesis.

Growth

Revenue: $8.07B

5Y Revenue Growth: 15.3%

Expected EPS Growth: 10.0%

Profitability

EBIT Margin: 29.8%

Net Margin: 22.3%

ROE: 43.4%

Most automakers operate with single-digit operating margins.

Ferrari generates luxury-level returns.

Cash Flow & Balance Sheet

Debt/Equity: 0.76

Current Ratio: 2.3

This is not a capital-destroying industrial business.

It is a high-return brand platform.

Valuation: Premium for a Reason?

Ferrari trades at:

P/E: 37.5

Forward P/E: 30.4

EV/EBITDA: 22.9

P/FCF: 32.4

Expensive compared to traditional automakers.

But the comparison may be wrong.

The market is not assigning an auto multiple.

It is assigning a luxury multiple.

The real debate is not whether Ferrari is cheap.

The debate is whether Ferrari deserves to be valued like a long-term luxury compounder.

Growth Drivers

Ferrari still has multiple levers:

Price increases

More premium model mix

Limited editions

Hybrid and upcoming electric models

Growth is driven more by value per car than units sold.

Order books often extend years ahead, giving strong revenue visibility and reducing cyclicality relative to mass-market peers.

Key Risks

Premium valuation leaves little room for error

Electrification could challenge brand identity

Ultra-luxury demand depends on global wealth conditions

Ferrari is not immune to cycles, but it is structurally more insulated than traditional manufacturers.

Investment Question

Ferrari combines:

Scarcity

Brand power

Pricing strength

Industry-leading margins

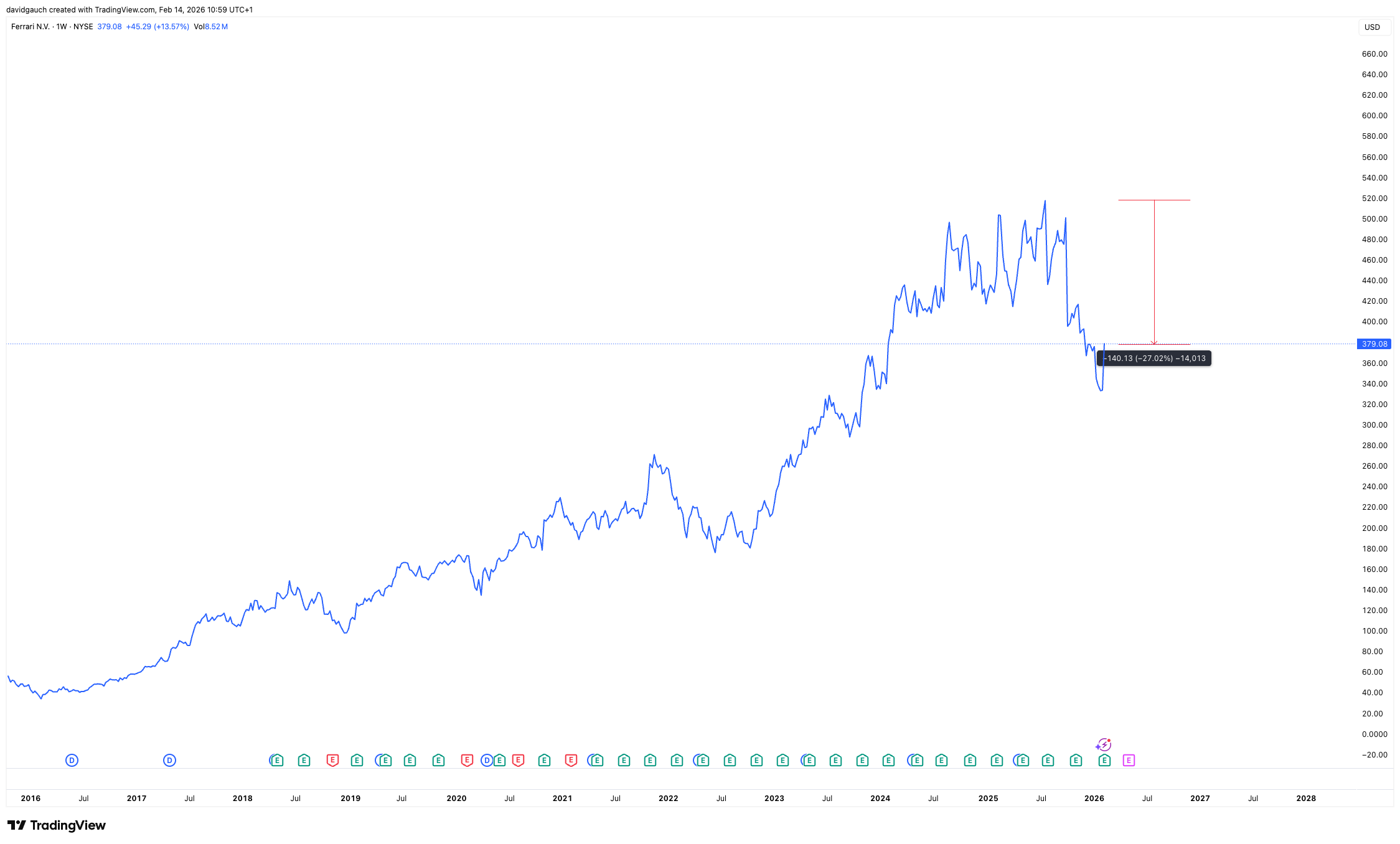

In my view, Ferrari could offer attractive diversification for a global portfolio, especially with the stock trading around 27% below its previous all-time high.

As always, this is not financial advice. The goal of Alpha Bets is to share ideas, frameworks, and investment theses, not to provide buy or sell recommendations. Every investor should do their own research and make decisions based on their personal risk tolerance, time horizon, and financial situation.

P.S. If you own $RACE, you can tell your friends you own Ferrari.

Just not one in your garage.

David Gauch

Founder, Gauch Research