2025 Year in Review

Noise, Uncertainty, and the Case for Process

My Performance This Year:

I started the year deliberately cash-heavy, anticipating elevated volatility around Trump’s inauguration and the potential for disorderly repricing. Rather than forcing early exposure, I waited for volatility to materialize and for price to define opportunity.

That patience paid off.

Once conditions aligned, capital was deployed selectively.

As a result, my core portfolio delivered a total return of 48%, materially outperforming broader market benchmarks.

This outcome was not driven by constant activity, but by timing, selectivity, and risk discipline.

Looking Back: What Defined this Year

2025 was not short on events. It was a year dominated by uncertainty, political shocks, and sharp repricing phases across assets.

Key developments included:

The DeepSeek selloff, triggering a brief but violent risk-off move

Trump’s inauguration and the immediate shift in trade rhetoric

Liberation Day and renewed tariff threats

Ongoing Federal Reserve credibility drama

Further rate cuts amid slowing labor dynamics

A government shutdown adding fiscal stress

And, despite all of this, huge market moves

The dominant feature of the year was not direction, it was uncertainty.

Look at the Numbers

What truly defined 2025 was the level of macro noise. This was most clearly reflected in gold and silver, both of which acted as real-time barometers for uncertainty and confidence in monetary policy.

The result: deeply polarized market views.

Recession calls were everywhere. High-profile investors openly positioned for economic contraction, Michael Burry being one of the most notable examples.

Yet despite the constant headwinds, the market remained resilient.

As of now, equities are up roughly 17% on the year.

That disconnect between narrative and price should be the key lesson of 2025.

Why Data Matters in Noisy Environments

During periods like this, I deliberately narrow my focus to hard data.

Not opinions.

Not headlines.

Not narratives.

Because when uncertainty is high, many market participants lose perspective, they miss the forest for the trees. I’ve made that mistake myself.

So let’s walk through the data and draw conclusions from what actually matters.

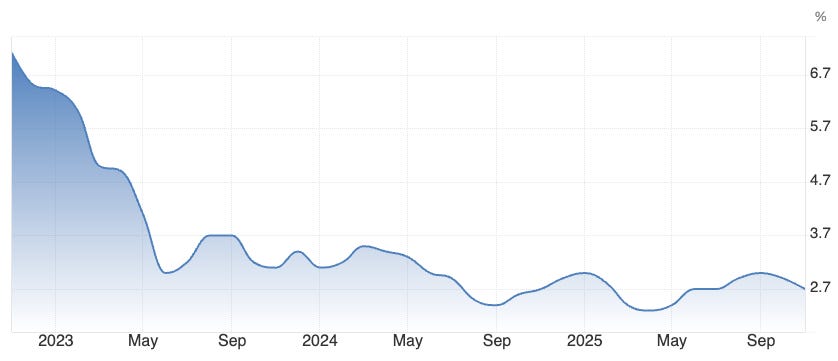

Inflation: 2.7% YoY

Despite a temporary uptick during summer and early autumn, largely driven by newly introduced tariffs under the Trump administration, the long-anticipated delayed inflation shock never materialized.

Last week’s inflation data came in significantly below expectations, even if some argue the figures understate underlying pressures.

Still, the trajectory remains clear: inflation continues to move toward the Federal Reserve’s 2% target.

Whether that target is ever reached exactly is secondary. Direction matters more than precision.

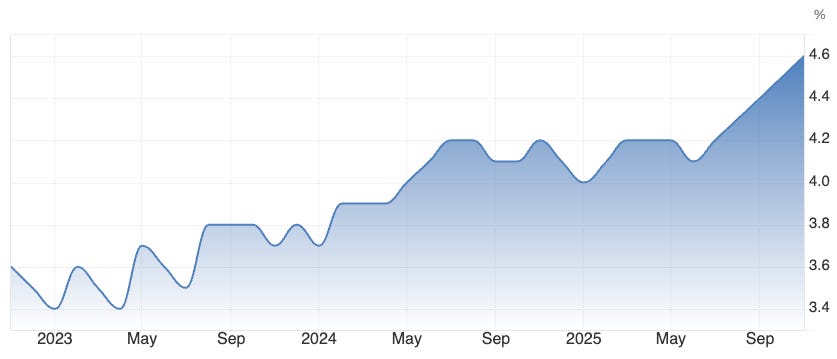

Unemployment Rate: 4.6% YoY

The effects of quantitative tightening and the government shutdown are now visible in the labor market.

The question is no longer if the labor market is weakening, it is.

That said, conditions remain historically manageable. This is not a crisis. But the deterioration is meaningful.

At 4.6%, unemployment now exceeds the Fed’s own projections for 2026, adding pressure to an already complicated policy backdrop.

This materially shifts the balance within the Fed’s dual mandate.

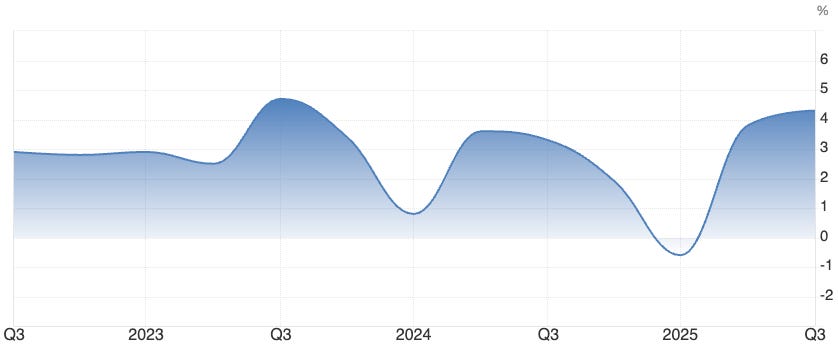

GDP Growth: 4.3% YoY

GDP data this year has been volatile, and misleading if taken at face value.

Much of the distortion stems from tariff front-loading, as companies accelerated imports ahead of tariff implementation. This artificially boosted imports earlier in the year and subsequently dragged GDP sharply lower during the summer.

The takeaway:

Headline GDP swings overstated both strength and weakness.

The underlying economy slowed, but did not collapse.

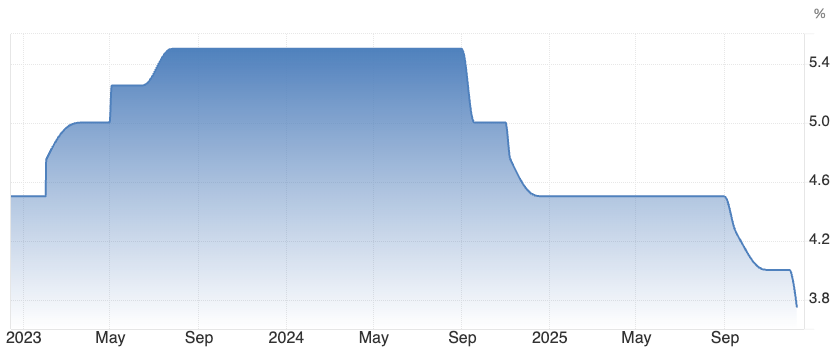

Interest Rates: 3.50%-3.75%

When we step back and focus strictly on the Federal Reserve’s mandate, balancing inflation and employment, the policy path becomes clearer.

With inflation trending lower and labor markets softening, further rate cuts in 2026 remain likely.

Our base case expects 50–75bps of additional easing toward neutral, which would:

keep pressure on the USD

support short-duration bonds

and steepen parts of the yield curve

Outlook: What Comes Next?

USD: Structural Headwinds

From a macro perspective, the data continues to point toward further USD weakness.

Looking ahead to 2026:

A new Fed Chair is expected

Policy is likely to turn more dovish, aligning more closely with the current administration

The unresolved US debt burden remains a long-term risk, particularly for long-dated yields

This combination is not supportive for sustained dollar strength.

EUR: A Case for Relative Recovery

If we have a directional bias on the USD, we need a credible counterweight.

In most cases, that counterweight is the euro.

Europe has had its own challenges this year, but several developments are constructive:

A new government framework

Large-scale infrastructure investment plans

A central bank that has already moved rates toward a possible neutral level

Stabilizing inflation

A labor market that remains resilient

Taken together, conditions increasingly point toward relative recovery in the Eurozone, particularly versus the US.

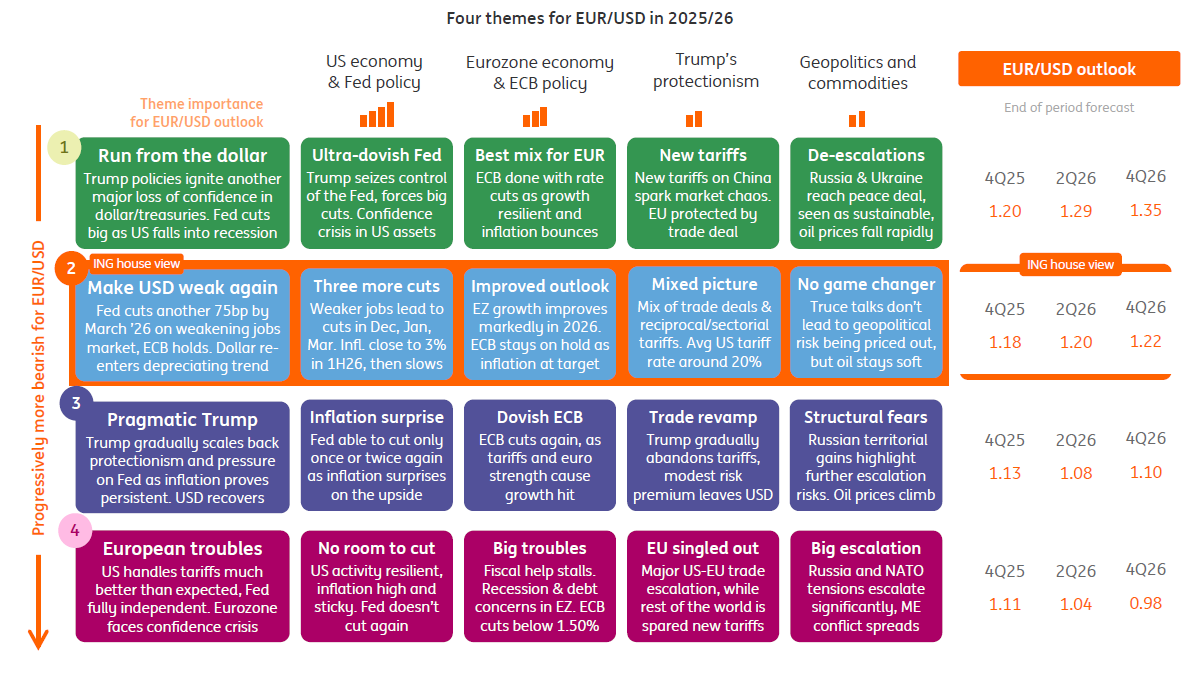

ING’s potential scenarios:

Process Going Forward

Going forward, all analysis will be structured around the SVC-Framework:

Structure → Validation → Context

Structure: Price defines direction

Validation: Macro data determines durability

Context: Sentiment and positioning define conviction and timing risk

No structure → no trade.

No validation → fragile conviction.

No context → unmanaged risk.

This framework enforces clarity, discipline, and consistency, especially in noisy market environments.

What This Means for Gauch Research Readers

SVC allows for concise, structured, and transparent market analysis.

Each update is designed to deliver:

a clear directional bias

an explicit conviction level

and defined risk conditions

All within minutes, not pages.

The goal is not to overwhelm with data, but to filter what actually matters.

Premium Access & Depth

While public updates focus on direction and conviction, deeper layers remain intentionally reserved.

For Premium subscribers, this includes:

detailed fundamental breakdowns

full macro validation logic

and access to my proprietary analytical tools via Atlas-Terminal

This structure ensures that:

free readers receive clear, actionable market context

premium members gain depth, transparency, and implementation-level insight

Value is created through process, not volume.

SVC is not designed to predict markets.

It is designed to remove noise, enforce discipline, and improve decision quality.

That standard defines Gauch Research going forward.

Wishing you a successful year ahead,

David Gauch

Founder, Gauch Research

Wow, great article!!

Loved the clarity in the high level ideas.

Looking forward to continuing to read your newsletter.